It’s a homeowner’s dream: You purchased your home and its overall value is hockey sticking. For Greater Boston residents who’ve owned their home for around 7.5 years, there’s no hyperbole since during that time home values have increased 28%.

But like all homeowners, you must continuously maintain your property. Many are wondering if the upside of a high home value is worth the stressful downside of keeping up the interior and exterior. Read on for guidance on how to approach the decision to stay put or sell.

The Onus of Homeownership

Whether you’re a first-time owner or in your second or third home, the responsibilities of homeownership are perennial. From small, everyday fixes to annual maintenance or surprise repairs, a home is a living thing that needs regular care and attention.

According to a recent Hometap survey, home maintenance and upkeep costs are the biggest source of stress for Greater Boston residents. Nearly three-quarters of those polled identified the tasks surrounding upkeep—landscaping, cleaning, routine home repairs, leaf and snow removal—as nerve-wracking while 63% are worried by the costs associated with maintenance tasks.

How to Get Ahead in Homeownership

The good news for Greater Boston owners is you’re likely sitting on hundreds of thousands of dollars in equity. And the cherry on top is that no slowdown in home values is anticipated in the future. (That might be cold comfort for some faced with major repairs or renovations on the horizon.)

Before you put up the “for sale” sign, consider all your options.

1. Plan Ahead

Do you have a plan of attack for regular maintenance and a smart savings plan? If not, see our expert tips on how to get one started today. It’s easier than you might think.

2. Cut Costs on Your Renovation

The kitchen or bathroom remodel is unavoidable. But cutting costs before and even during your project is doable—without cutting corners. Check out our 10 not-so-secret ways to reduce your renovation expenses.

3. Tap Into Your Home’s Equity

Some homeowners rely on smart solutions like a Hometap Investment to “cash in” on their home’s value. With no monthly payments or interest, Hometap offers homeowners a way to fund the present without risking their future. Learn more about Hometap.

How Much Is Your Home Really Worth?

For many Americans, their home is the biggest purchase they’ll make in their lives. Staying in—or selling—your home is a personal decision with emotional and financial consequences. If you love your neighborhood, your community, and the commute to work, staying put might have more value than you realized. An upswing in your home value is an added perk, too. With a small-step, reduced-stressed approach to upkeep and smart financing, you can stay in your home as long as you choose.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

A reverse mortgage allows homeowners who are at least 62 years old to use home equity to supplement their retirement income. Reverse mortgages, also called home equity conversion mortgages, aren’t like conventional forward mortgages in that you do not make monthly mortgage payments. So, how does a reverse mortgage work?

Instead, as ReverseMortgageAlert.org describes, “the borrower receives payments from the lender and does not need to make payments back to the lender as long as he or she lives in the home and continues to fulfill basic responsibilities, such as payment of taxes and insurance.” As time goes on, the loan balance and interest grows, while home equity decreases.

While this option was perhaps an afterthought for many retirees in the past, the coronavirus crisis has brought it to the forefront once again as a choice for those whose funds were decimated during the economic crash caused by the pandemic. Applications for home equity conversion mortgages (HECMs) increased 15% in March 2020 from the previous month, and up 50% in Q1 from 2019.

“Our customer is the older homeowner that is in their retirement, and their retirement just got pummeled by about 20% or 30%,” he explained. “Our customers are thinking, ‘I should be accessing the equity in my home versus trying to sell off my position or live off my retirement with the notion that over time, it’ll come back.”

Experts believe that the knowledge deficit that existed when reverse mortgages first hit the market has been addressed, leading to fewer cases of cold feet.

“Over the years, what I’ve noticed, especially with borrowers in that 62 to 72 range now, they’re coming in a lot more educated than they had previously been on the product,” Paul Fiore, chief retail sales and operations officer at AAG, told HousingWire. “They’ve done a lot of research, probably online, looked into different things and different aspects of the product. So, they’re coming in more educated, at least in the fundamentals of the loan.”

There are three types of reverse mortgages:

Single-purpose reverse mortgages

This option is typically the least costly, but it has restrictions and might not be the easiest to come by. As the name suggests, the lender dictates the purpose of the loan — for example, to pay property taxes or take care of home repairs. While the qualification criteria makes it fairly easy for most homeowners with low-to-moderate income to get approved, they aren’t very widely available, mainly offered by state and local governments and select nonprofits.

Proprietary reverse mortgages

These are private loans that are funded by the companies that create them. This may be a better choice if you own a high-value home, as you have the potential to receive a higher loan amount than you would with other types of reverse mortgages, especially if your mortgage balance is low.

Home Equity Conversion Mortgages (HECMs)

HECMs are backed by the U.S. Department of Housing and Urban Development (HUD) and are federally insured. There are a few advantages to HECMs: there isn’t a firm income requirement, and unlike single-purpose mortgages, they can be used for any reason. However, they tend to be pricier than old-fashioned home equity loans in terms of both total costs and upfront fees.

Reverse Mortgage Pros

No mortgage payments. A reverse mortgage allows retirees on fixed incomes to stay in their home — with no monthly mortgage payments. The entire loan comes due at the end of the term, generally when the homeowner dies or moves out.

Immediate cash. Many families have little to no retirement savings, according to the U.S. Government Accountability Office. If you’re in a similar boat but have equity in your home, a reverse mortgage can help eliminate or mitigate cash flow issues that can crop up once you’ve stopped working.

Bigger Social Security benefits. A reverse mortgage can allow you to delay drawing on your Social Security, helping you reap bigger benefits down the road. As the Internal Revenue Service lays out, you can get 100% of your benefits at age 66. But you can get 132% of your benefits if you wait to draw funds until age 70.

See how Reverse Mortgages compare to home equity loans, refinances, and other financial products in our Home Equity Investments 101 Guide.

Reverse Mortgage Cons

High fees. According to Reverse.org, reverse mortgage fees are typically higher than those of a traditional mortgage. For example, there’s an initial Federal Housing Administration (FHA) mortgage insurance premium of 2% of the home value, up to $13,593, plus ongoing FHA premiums of 0.5% of the outstanding mortgage balance.

Inability to move. You may not have plans to move. But, as Investopedia cautions, if you have to move into a nursing home or assisted living facility for more than 12 consecutive months, it’s considered a permanent move. Since lenders require you to live in the home you’re borrowing against, you’ll need to pay back the reverse mortgage. If you can’t, then the lender will foreclose on your home.

“When the money runs out, you can’t borrow any more. You can’t dip into that well,” warns Bruce McClary of the National Foundation for Credit Counseling. “And often times what happens is this leaves seniors with their back up against the wall with one less financial option and a home to maintain…it is a back pocket option, and I would say that people should probably save it as something that’s more like a last resort.”

Inheritance is tricky. If you’re hoping to keep your home in your family, your heirs will have to repay the loan balance. Reverse Mortgage Funding says that the loan is traditionally paid off by selling the home or refinancing through a traditional mortgage.

“There are provisions that allow family to take possession of the home in those situations, but they must pay off the loan with their own money or qualify for a mortgage that will cover what is owed,” McClary adds. And while a reverse mortgage refinance is possible, it’s quite uncommon and requires that very specific criteria be met first.

Alternatives to a Reverse Mortgage

Reverse mortgages aren’t your only financing option as a homeowner. Unlike reverse mortgages that require you to be 62 years or older, these financing options do not have age restrictions. Plus, you don’t have to fully own your home (or have a very small mortgage) to qualify as you do with a reverse mortgage.

Home equity instruments. A home equity loan and a home equity line of credit (HELOC) are not the same thing. Although both allow borrowing against the equity in your home, the terms differ. A home equity loan is a lump sum that generally has a fixed rate while HELOC rates are usually adjustable and the amounts are smaller. Both are better suited to filling short-term financial needs.

In addition to considering your long- and short-term financial needs, you’ll want to determine the cost of borrowing, taking into account interest and fees.

Selling your home. If you sell your home — particularly if your mortgage is paid off — and move to a rental property, you can gain a significant bump to your retirement fund. Downsides include monthly rent payments and the loss of property from your estate.

Hometap. For many homeowners, Hometap can offer the best of both worlds. Like a reverse mortgage, a Hometap Investment eliminates monthly payments. But because Hometap is an investment, not a loan, it could be the most affordable option, as you don’t have to worry about paying interest, either.

Unlike some reverse mortgage options, there aren’t any restrictions on how you can use the money, so you can put it toward whatever is most important to you, from renovating your home, to paying down debt, or diversifying your portfolio. Finally, if you’re worried about qualifying for a reverse mortgage, it may help to know that the requirements for a Hometap Investment are unique from a reverse mortgage and traditional loan options.

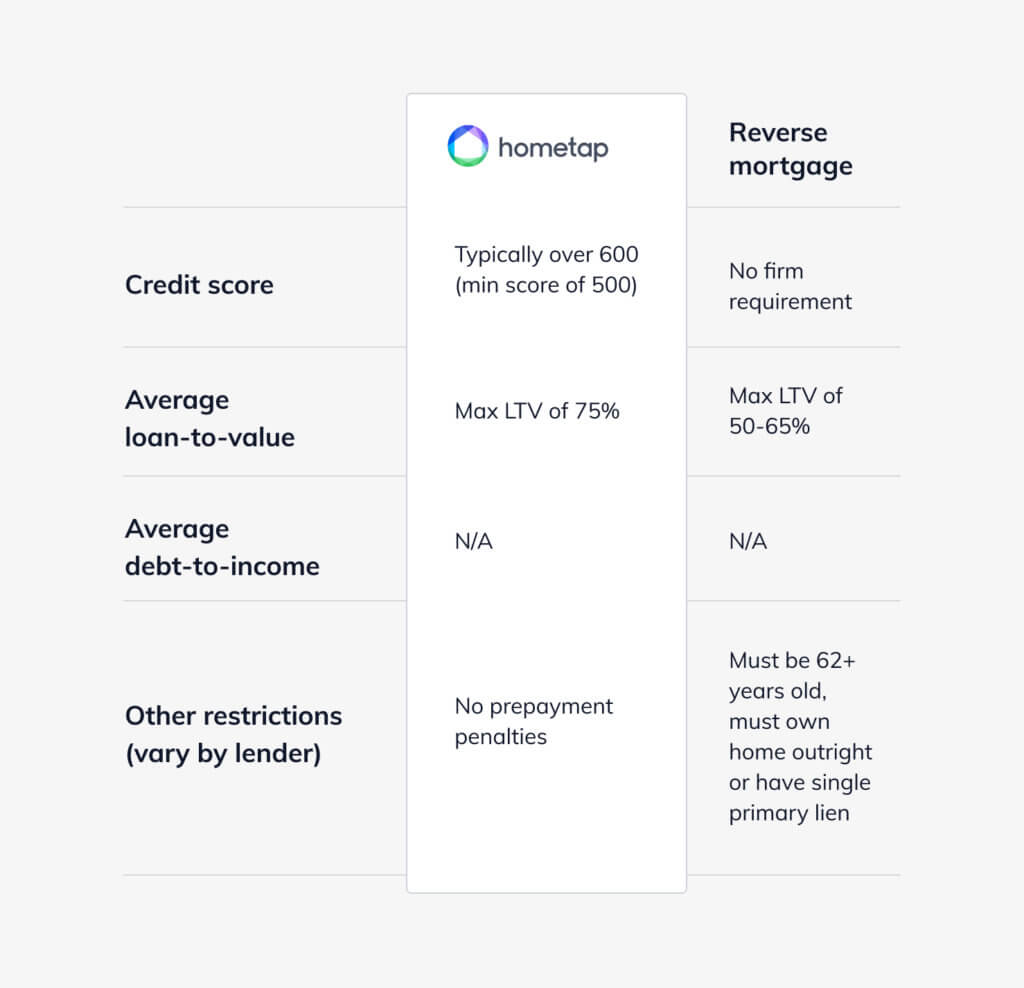

You can quickly compare a Hometap Investment and a reverse mortgage using the chart below.

Everyone hopes they’ve set aside enough money to enjoy retirement, but unexpected expenses or a longer lifespan may leave us needing additional sources of income. Carefully consider the pros and the cons of a reverse mortgage to decide where your home fits into your retirement plan based on your goals and your situation.

Take our 5-minute quiz to see if a home equity investment is a good fit to fund your financial goals.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

With rising taxes, Medicare costs, and interest rates, retirement doesn’t come cheap. More than 1 million reverse mortgages, or Home Equity Conversion Mortgages, have been sold since 1990. But before you decide to fund your retirement via a reverse mortgage, it’s worth weighing the benefits against the risks for your situation, plus exploring alternative ways to fund your retirement dreams.

When to Apply for a Reverse Mortgage

1. You Want to Grow Your Retirement Savings

Since reverse mortgages offer fast cash, you can add that money to your retirement savings. The extra cash allows you to diversify your portfolio and grow your future funds.

2. You Can Cover Closing Fees

As with traditional mortgages, reverse mortgages have their own closing costs. According to American Advisor Group, fees include:

Credit Report: $20–$50

Flood Certification: $20–$30

Escrow Fee: $150–$800

Document Prep: $75–$150

Recording: $50–$500

Courier: $50

Title Insurance: Varies by loan amount and region

Pest Inspection: $100

Survey: $100–$250

You’ll also pay an initial mortgage insurance premium fee equal to 2% of your home’s value, plus a loan origination fee charged by your lender starting at 2% of the loan with a maximum of $6,000. It’s possible to roll many of these costs into the reverse mortgage itself, but a home appraisal—$400–$600—must be paid upfront.

When to Steer Clear of a Reverse Mortgage

1. You May Need to Leave Your Home

Reverse mortgages are not forgiving if unexpected health issues arise. That means if you need to move into a nursing home or assisted living facility, the loan will need to be paid upfront. (A leave of absence longer than 12 consecutive months is considered a permanent move by law.)

It’s difficult to plan for future illness. Take the time now to ask yourself the tough questions about if or when you’d need to leave your home.

Reverse mortgages have no monthly payments, but they do require homeowners keep up with other related costs. These range from home maintenance, property tax, and insurance. Unfortunately, more and more seniors are facing foreclosure from reverse mortgages because they fell behind or failed to meet other requirements.

Alternative Retirement Funding Options

1. Personal Loans

Personal loans are beneficial for paying down debt in a number of ways. Not only will your credit score rise from lowering your debt but you can apply for a lower-rate reverse mortgage later if it’s a fit to fund your retirement.

2. Equity Investments

Home Equity Investing is exactly what it sounds like. Homeowners tap into their home’s equity in exchange for a share of the property’s future appreciation or depreciation.

A Hometap Investment is an equity investment that allows you to fund your retirement and stay in your home—without any monthly payments or interest. And unlike other options, you don’t need to sell your home when your term ends; you can refinance or buy out the Investment with savings instead.

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

The average home renovation project lasts six to eight months and involves around 15,000 decisions. Sometimes hiring a professional to guide you, keep you on track, and make some of those decisions is worth the investment.

A home renovation consultant, also referred to as a home renovation coach or a home improvement consultant, is essentially an expert project manager for your home remodel or renovation. But what exactly does a home renovation consultant do and do you need one? Read on as we explore a typical consultant’s role and the types of projects that benefit from one.

What Is a Home Renovation Consultant?

A home renovation consultant advocates for you and your project by hiring and managing the right people for your renovation job. This professional isn’t a contractor or architect but rather helps with the budget, design, vendor meetings, and/or material selection. They may guide you from start to finish or put you in the right direction.

While costs vary depending on the consultant and the project, Realtor.com spoke with several professionals and found base packages starting around $250 for initial design consultations. Larger projects, like a complete kitchen remodel lasting two to three months, can cost anywhere from $3,000 to $5,000.

When to Hire a Renovation Consultant

When is it worth it to spend $250 to $5,000 or more? Larger projects that require multiple vendors are a prime example of when a home renovation consultant can save you time and possibly money in the long run.

Rather than carving out the time to manage multiple vendors on your own, the home improvement consultant can provide you with unbiased advice and connect you with professionals suited to your project. By giving you a realistic picture of what it’ll take to complete the project and connecting you with the right people upfront, the renovation consultant can save you from costly do-overs and mistakes.

If you have trouble staying on budget, you may want to consider a renovation consultant. The consultant can develop a realistic budget at the beginning of the project so you know what to expect rather than later facing a half-completed project and vendors telling you it’s going to cost more than anticipated. This person can also keep the project on task, ensuring vendors—and you—are always working toward your ultimate end goal versus getting sidetracked.

One of the most valuable things a home renovation consultant can bring to your project is their network of trusted vendors, from architects and general contractors to designers and materials specialists. If you don’t know what professional(s) to hire for what portion of your project, you can hire a consultant to point you in the right direction.

When You Can DIY

If your budget is tight and you can reasonably find time to manage the project, then you may consider forgoing the services of a renovation consultant. However, you may find it’s worth making room in your budget for a renovation consultant if only to ensure you’re plotting a course that will get the project done right the first time—and keep you within budget.

Small, weekend jobs also don’t warrant a renovation consultant. Of course, if the job ends up going off the rails in a weekend, it’s not too late to hire a renovation consultant to assess the situation, mitigate any disputes, and provide you with the most cost-effective path for getting your project back on track.

Before you assume that you can cut corners and forgo the initial cost of a renovation consultant, take a step back from your project. Do you know what kinds of professionals you need for your project? Do you have a professional you trust? Could you have blind spots that would benefit from an unbiased outside opinion? Sometimes the small, simple projects are the ones that can easily get off-track. The added upfront cost of hiring a renovation consultant may save you from unexpected costs later in the project.

Did you know the equity in your home could fund your renovation? Learn how home equity investments compare to renovation loans, lines of credit, and other solutions for funding your home remodel.

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

How much could you save on your mortgage with an improved credit score? A lot, it turns out.

According to BankRate, your credit score is one of the top factors that lenders consider when setting your interest rate. A solid score indicates to lenders that you present less of a financial risk and they reward that track record with generous loan terms. Credit.com reveals that loan officers also compare credit score and the loan-to-value ratio to determine interest rate adjustments.

It’s no secret that the closer your score is to 800, the odds of home loan approval go up and interest rates go down. But just how much of a score increase do you really need to see a significant difference?

Small Changes, Big Difference

On the vast scale of 800, a handful of points here or there may not seem like much. As such, most of us are focused on those big, hundred-point jumps that get us out of the garden-level apartment (500) and into the higher-rent districts (600, 700) or even the penthouse (800).

But it’s crucial to remember that the lending industry measures in 20-point increments and adjusts rates accordingly. This means a drop from 780 to 760 will likely result in higher costs that grow even higher for every level you go down. This system, as NerdWallet explains, is known as loan-level pricing. As 20, 40, 60 points start to rack up, you’ll find yourself talking about real money very quickly.

If your score drops by 100 points or more, the landscape can change completely. This is particularly true over the long view of 30 years when you may end up owing tens of thousands more in loan payments.

In short, your credit score is money. The better it is, the more you’ll have. It, therefore, pays off in the long run to be vigilant—handle debt responsibly, don’t spend beyond your means, and do your best to pay all bills on time and in full.

Whether you need a loan to consolidate debt or pay down bills, Hometap can be a smart option for homeowners looking to cash in on their equity without monthly payments or interest.

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.