When it comes to financing your home, one size doesn’t fit all. And while traditional options like loans, home equity lines of credit (HELOCS), refinancing, and reverse mortgages can work well for some homeowners, the recent rise of loan alternatives like home equity investors and other emerging platforms have made it clear that there’s a growing demand for other choices. Learn more about alternative ways to get equity out of your home, so you can make a more informed decision.

Traditional Options: Pros and Cons

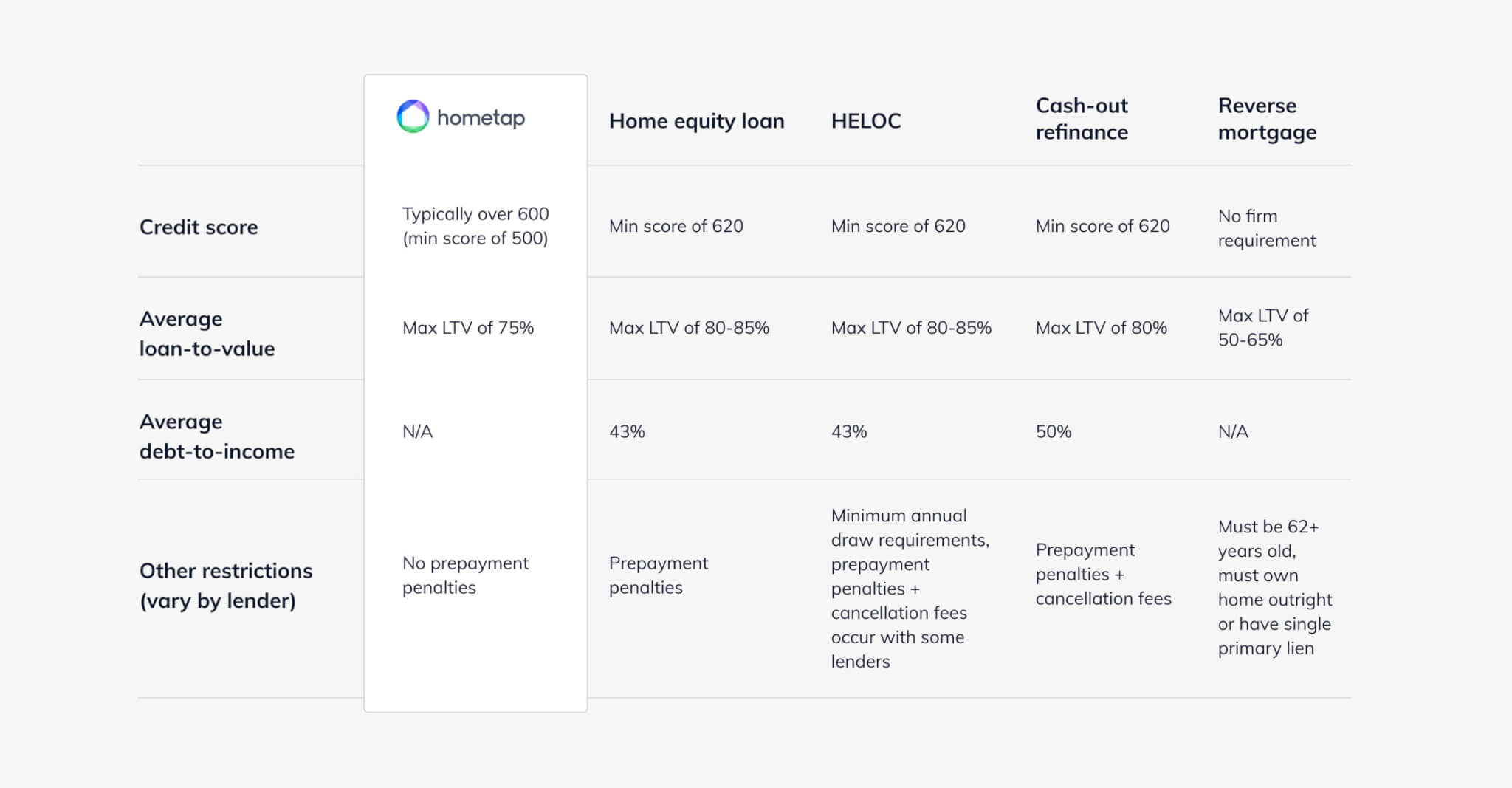

Loans, HELOCs, refinancing, and reverse mortgages can all be attractive ways to tap into the equity you’ve built up in your home. However, there are often as many disadvantages as there are benefits — so it’s important to understand the pros and cons of each to understand why some homeowners are seeking financing alternatives. See the chart below to quickly compare loan options, then read on for more details on each.

Home Equity Loans

A home equity loan is one of the most popular ways that homeowners access their equity. There are certainly advantages, including a predictable monthly payment due to the loan’s fixed interest rate, and the fact that you’ll receive the equity in one lump sum payment. For this reason, a home equity loan typically makes sense if you’re looking to cover the cost of a renovation project or large one-off expense. Plus, your interest payments may be tax-deductible if you’re using the money for home improvements.

Why search for a home equity loan alternative? A few reasons: First, you’ll need to pay off the loan in addition to your regular mortgage payments. And if your credit is less-than-excellent (under 680), you may not even be approved for a home equity loan. Finally, the application process can be invasive, cumbersome, and taxing.

Home Equity Lines of Credit (HELOC)

HELOCs, a common alternative to a home equity loan, offer quick and easy access to funds any time you need them. And while you typically need a minimum credit score of 680 to qualify for a HELOC, it can actually help you improve your score over time. What’s more, you might be able to enjoy tax benefits — deductions up to $100,000. Since it’s a credit line, there’s no interest due unless you take out money, and you can take out as much as you want until you hit your limit.

But with this flexibility comes the potential for additional debt. For example, if you plan to use it to pay off credit cards that have high interest rates, you can wind up racking up more charges. This actually occurs so frequently that it’s known to lenders as “reloading.”

Another major downside that may encourage homeowners to seek a HELOC alternative is the instability and unpredictability that comes along with this option, as the variability in rates can lead to fluctuating bills. Your lender can also freeze your HELOC at any time — or reduce your credit limit — in the event of a drop in your credit score or home value.

Discover how common it is for homeowners like you to apply for home loans and HELOCs, in our 2021 Homeowner Report.

Cash-out Refinance

One alternative to a home equity loan is a cash-out refinance. One of the biggest perks of a cash-out refinance is that you can secure a lower interest rate on your mortgage, which means lower monthly payments and more cash to pay for other expenses. Or, if you’re able to make higher payments, a refinance might be a good way to shorten your mortgage.

Of course, refinancing has its own set of challenges. Since you’re essentially paying off your current mortgage with a new one, you’re extending your mortgage timeline and you’re saddled with the same charges you dealt with the first time around: application, closing, and origination fees, title insurance, and possibly an appraisal.

Overall, you can expect to shell out between two and six percent of the total amount you borrow, depending on the specific lender. Even so-called “no-cost” refinances can be deceptive, as you’ll likely have a higher rate to compensate. If the amount you’re borrowing is greater than 80% of your home’s value, you’ll likely need to pay for private mortgage insurance (PMI).

Clearing the hurdles of application and qualification can lead to dead ends for many homeowners who have blemishes on their credit score or whose scores simply aren’t high enough; most lenders require a credit score of at least 620. These are just some of the reasons homeowners may find themselves seeking an alternative to a cash-out refinance.

Reverse Mortgage

With no monthly payments, a reverse mortgage can be ideal for older homeowners looking for extra cash during retirement; a recent estimate from the National Reverse Mortgage Lenders Association found that senior citizens had $7.54 trillion tied up in real estate equity. However, you’re still responsible for the payment of insurance and taxes, and need to stay in the home for the life of the loan. Reverse mortgages also have an age requirement of 62+, which rules it out as a viable option for many.

There’s a lot to consider when looking at traditional and alternative ways to access your home equity. The following guide can help you navigate each option even further.

Looking for an Alternative? Enter the Home Equity Investment

A newer alternative to home equity loans is home equity investments. The benefits of a home equity investment, like Hometap offers, or a shared appreciation agreement, are numerous. These investors give you near-immediate access to the equity you’ve built in your home in exchange for a share of its future value. At the end of the investment’s effective period (which depends on the company), you settle the investment by buying it out with savings, refinancing, or selling your home.

With Hometap, in addition to an easy and seamless application process and unique qualification criteria that is often more inclusive than that of lenders, you’ll have one point of contact throughout the investment experience. Perhaps the most important difference is that unlike these more traditional avenues, there are no monthly payments or interest to worry about on top of your mortgage payments, so you can reach your financial goals faster. If you’re seeking alternative ways to get equity out of your home, working with a home equity investor might be worth exploring.

Is a Hometap Investment the right home equity loan alternative for you and your property? Take our five-minute quiz to find out.

YOU SHOULD KNOW

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.