David Leveraged His Equity to Fund an Investment Property

It’s a good time to own property in the Grand Canyon State. Home values in Phoenix have grown faster than any other U.S. city year over year from 2019-2020.

With property values increasing at historic rates and an influx of people moving to the west side of Phoenix, David and his wife knew they had an opportunity to add another income stream in the form of an investment property — but only if they could act fast and obtain substantial capital given the increasingly competitive real estate market.

Having just recently refinanced, David knew he’d likely need to put their investment property plans on hold for a while to secure the funds with another refinance. But waiting meant watching the home prices grow and inventory shrink. That’s when David discovered Hometap.

“When I heard the [radio] ad, it was the first time I’d ever heard about that concept of selling equity and basically taking on a partner in my house,” said David.

David had been through the process of utilizing a home equity line of credit (HELOC) before, too, so knew he was looking at a 6-7% interest rate if he went that route.

Self-employed and working for the family business, the lack of a standard W2 could add another challenge to the refinance and HELOC application process. He continued to mull over his options.

“I couldn’t do a refinance because I just refinanced in September. It would have cost quite a bit to do a refinance within that period of time, even though the [home] value had increased,” said David. “And there wasn’t much chance of getting a better interest rate because it was already at 2.99%. Unless I was to move to a 15-year term…which in that case would have made my payment much higher than I would’ve wanted.”

After walking through several scenarios with his Hometap Investment Manager, David had made his decision. On top of being a solution with no monthly payments or interest, Hometap’s 20% annual appreciation cap and downside protection put him at ease.

“The Hometap route was attractive because of no ongoing payments, I had a view of opportunity costs and [I had an] underutilized asset. [That] was a motivating factor, as well as accessing the equity in a timely manner without tacking on additional monthly obligations.”

After a few weeks, David and his wife closed on a Hometap Investment and began shopping for their investment property.

You’ve heard the term, but what is home equity, exactly, and how is it calculated? Home equity is the value of a homeowner’s interest in their home, and it’s important to keep track of because home equity provides opportunity for homeowners. This number changes over time due to both market shifts like local and national trends, as well as your own mortgage payments; the more you’ve put toward your home, the more equity you’ll have. Here we’ll cover how to calculate home equity, and how to use it.

Why Is Home Equity Important?

Building equity in your home is important for a few reasons. First, it counts toward your net worth because unlike nearly every other asset you buy with a loan, your home can still grow in value after you pay it off. You can also borrow your equity to handle life expenses like home renovations, a down payment on a second home, or to fund education — more on this later. Finally, when it comes time to sell your home, the more equity you’ve built up, the more profit you could make on the home.

How Long Does It Take to Gain Equity in a Home?

While there are factors that can expedite how quickly your home accrues equity (like the market shifts we mentioned previously), home equity does generally take time to build, so it should be part of a long-term wealth strategy rather than a short-term plan to get cash.

Homeowners that don’t know how much equity they have are also less likely to know how much debt they have. See more insights like this in our free Homeowner Report.

What is the Formula for Home Equity?

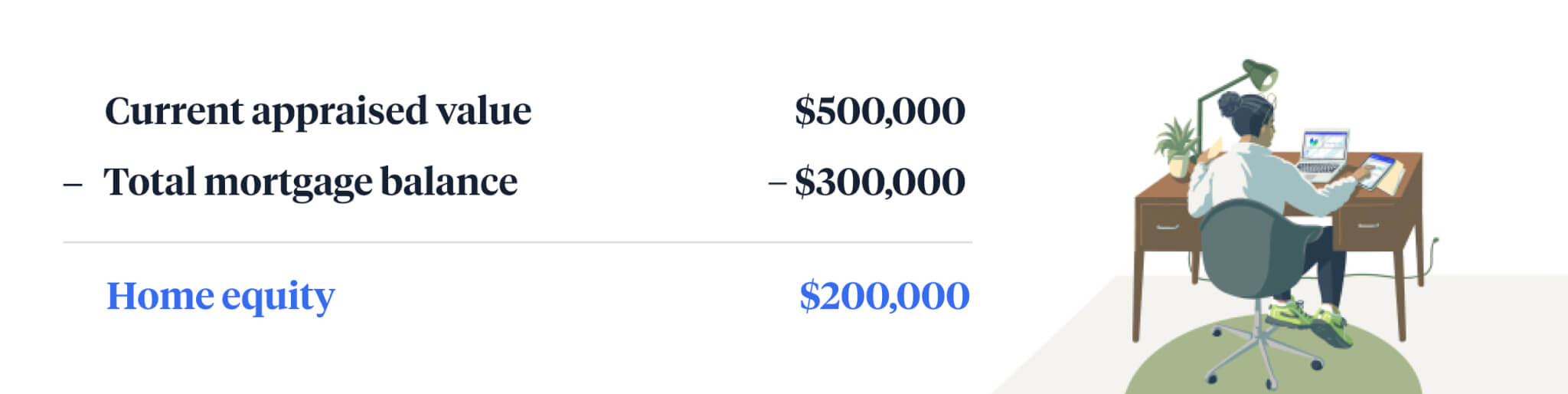

Fortunately, you don’t need a fancy home equity calculator to figure out how much equity is in your home. To find your home equity, simply subtract your total mortgage balance from the current appraised value of your home.

How to calculate home equity:

If you’ve been in your home for a while and aren’t quite sure of the current appraised value, there are a few different ways to go about determining it, short of scheduling a formal appraisal. You can start by looking at nearby “comps,” or comparable homes in your area that have similar square footage, number of bedrooms and bathrooms, and floor plans.

You can also look at the cost-per-square foot of your home and find an average. This is also pretty easy to do: simply divide the selling price of your home by the total square footage.

Once you have a general idea of your home’s current appraised value, you can subtract your mortgage balance to find your home equity.

If you’re curious about the rate at which your home might change in value over time, a home appreciation calculator can help.

How Can I Access My Home Equity?

Now that you know how to determine your home equity, it’s just as important to know to access it. There are several paths to tapping into your home equity, and each comes with pros and cons. Here are some of the most common ones:

Home equity loan

A loan thatoffers a predictable monthly payment, fixed rate, and a lump sum payment.

Home equity line of credit (HELOC)

A revolving line of credit that gives you access to cash through a portion of the equity you’ve built in your home.

Cash-out refinance

A mortgage that replaces your existing one and exceeds your loan balance, providing the difference in cash.

Reverse mortgage

A loan for homeowners 62+ in which the lender pays the borrower in exchange for the home’s equity.

How Can I get Equity Out of My Home without Refinancing?

There is one more financial product that doesn’t involve loans or refinancing your home, which means you can keep your interest rate locked in without adding another mortgage or another debt to your bottom line.

Home equity investments

This loan alternative gives you near-immediate funds in exchange for a share of your home’s future value without having to sell your home or take on more debt. There are no monthly payments and no interest.

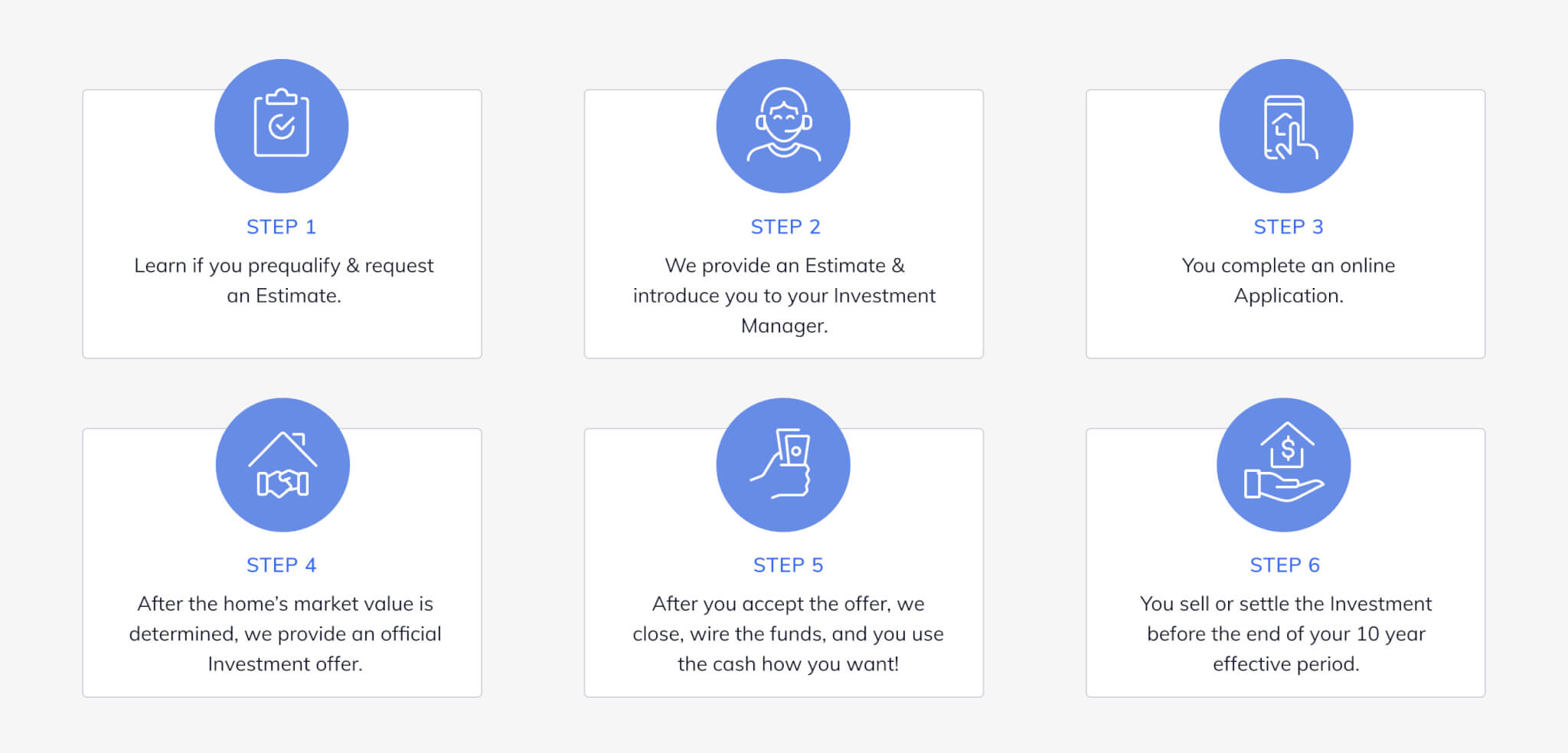

See how a Hometap Home Equity Investment works below:

How Much Equity Can I Borrow From My Home?

This answer will vary slightly depending on which financial product you choose to access it, but generally you’ll need to maintain at least 15-25% of your home equity. For example, if you have 50% equity in your home now, you’ll likely find that you’re able to receive 25-35% of it.

How Can My Equity Work for Me?

While there are many ways to use your home equity — and a home equity investment lets you use it for anything you’d like — it can pay off in the long run to be thoughtful and strategic about where you decide to put the funds you receive. For example, using the money to make home improvements that will potentially add more value to your home is probably a wiser decision than spending all of it on a lavish vacation or a shopping spree. Here are some possibilities to consider:

Pay Off Debt

Paying down debt, including credit cards and student loans, is one of the biggest reasons why homeowners access their equity. And with a home equity investment, this can be even easier to do, since there aren’t any monthly payments to deal with.

Renovate Your Home

Another common use for equity is home improvement and renovation projects. The benefits of this are a few fold: first, you’ll have the satisfaction and enjoyment of that dream kitchen or pretty patio. As we mentioned above, it’s also possible that the renovation will allow you to receive more money for your home if you decide to sell down the road.

Buy a Second Home

Have you always dreamed about a vacation home? How about an investment property that brings in additional income? You can put your equity toward a down payment on a second property. Besides having a go-to getaway spot, you’ll be diversifying your portfolio with real estate as well.

Fund Your Business

Many homeowners use their home equity to start or grow their small business without the hassles of a loan (and the hurdles that come along with getting approved for one).

Live Comfortably in Retirement

If you’re looking for a way to fund current — or future — expenses that your retirement savings can’t cover, like health care, your home equity can save the day and give you peace of mind, along with some extra cash. This is especially attractive if you plan to sell the home within the next 10 years. Though it isn’t required to sell, it may be beneficial to use the proceeds from the sale of the home to settle the Investment.

Fund an Education

With college tuition increasing every year, it can be a smart move to tap into your equity to help pay for your child’s education or start to chip away at that student loan debt.

Diversify Your Portfolio

Many homeowners use home equity investments to balance out their portfolio. A well-rounded portfolio includes a variety of investments that span across at least a few different sectors, including stocks, bonds, mutual funds, and real estate. By distributing your assets, you decrease the risk of a major loss in any one particular area.

Life is full of unexpected events. Whether you need cash, fast, to pay for medical bills, or deal with other surprise costs that pop up, your home equity can get you money in a pinch.

These are just some ideas for how you can use your equity to live a less stressful life — and a home equity investment can help you do it without taking on debt, worrying about monthly payments or interest, or having to sell your home. Now that you know how to calculate your home equity, what it is, and why it’s important, it’s time to decide how you’ll use it!

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

With its close proximity to Washington, D.C., Maryland is an especially popular place to live for many in the government and educational sectors. Situated along the Chesapeake Bay, the state is also home to healthy fishing and tourism industries and boasts beautiful waterfront properties that demand top dollar.

In fact, a study that looked at Maryland home prices from March to September of 2020 found that the 21056 zip code, the exclusive community of Gibson Island in Anne Arundel County, was one of the most expensive in the country, with a median home price of $1.95 million.

A recent Realtor.com study found that the state’s “hottest” zip codes were located between D.C. and Annapolis in the towns of Bowie, Columbia, and Crofton. While affordability was the primary driver of a high amount of home searches and quick sales, education and short distance to bigger cities also factored into the popularity of these suburbs.

Bustling Baltimore has plenty to offer, with the shopping and dining of the Inner Harbor, a world-class aquarium, and Fort McHenry, where the U.S. national anthem originated. In Baltimore, demand is strong: time on the market recently hit a historic low of just nine days. In contrast, that number was 27 days last year. The median home price here is currently $162,197, a 7% increase in the past year.

Still, it’s well below the statewide figure of $322,000 in November 2020, a decade high and a 32% increase year over year. However, the inventory was down 56% from the same month in 2019. In fact, at the height of the pandemic’s first wave in April 2020, home listings in the Baltimore metro area reached the lowest levels in 10 years at 3,628.

A City Surge

Closer into D.C., the prices are much higher. In the city of Potomac, the median closing price for a single-family home in September 2020 was $1.1 million. In Montgomery County, which includes Bethesda and Gaithersburg, the median price was $660,000, the highest it has been in 10 years. In Bethesda specifically, the median sold price for a detached/single-family home in June of 2020 was $1,110,000, a 5.7% jump year over year, and the city took the top spot in a December 2020 study from GOBankingRates that ranked the most overpriced cities in the country as based on the difference between home values and listing prices.

“If [you’re] going to telework, why pay high taxes in areas such as Montgomery County when you can do your job from Washington County, get a larger home in a less densely-populated area?” Leanne Kuehnle, a real estate agent in Hagerstown, told WDVM. “It’s very attractive to many new home purchasers.”

At the same time, there are fewer homes on the market than usual: while a typical January sees 900–950 listings in Frederick County, there were only 316 as of January 6, 2021. Compounding this is that many are homes yet to be built.

“It’s our understanding that even new construction, they’re having a hard time bringing houses to the market as quickly as they would like to because of COVID, because the factories are experiencing delays,” Realtor Cassandra Bailey told the Frederick News-Post.

Contrary to popular belief, you don’t need to sell your home — or even refinance it — to reap the benefits of its appreciation. Whether you’re looking to renovate, purchase a second property, or eliminate debt, a home equity investment gives you near-immediate access to the equity you’ve built without interest or monthly payments. If you’re a Maryland homeowner who’s looking to make the most of your home’s value, it might be the perfect time to start taking steps to make it happen and get closer to your financial goals.

Take our five-minute quiz to see if a Hometap Investment is right for you.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

A new breed of financial technology firms is pitching American homeowners on a different way of tapping into home equity. If you’re sitting on a pile of it, these companies — including Haus, Hometap, Noah, Point and Unison — will buy a piece of your house. You repay the “co-investment” when you sell.

So your application for a Small Business Administration (SBA) loan was denied. Unfortunately, you’re not alone.

If you’re a small business owner, an SBA loan can be a lifesaver, providing you with the funds you need to get — or stay — up and running, offering up to five million dollars for capital and expenses. There are a few different loan types that cater to different types of businesses, including 7(a), 504, and microloans.

The only problem? The restrictive criteria makes it quite difficult to qualify for a business loan in the first place. The approval rate can be as low as 25% at some banks. It’s easy to see why the top reason businesses fail is cash-flow, and 30% of small businesses are forced to call it quits in year two. Understanding why your application was rejected and what steps you can take to secure funding are key to your business’s success.

Reasons your application for an SBA loan was denied can run the gamut from more obvious ones to others that might not be so apparent. Some members of the Hometap team have experienced the small business loan application process firsthand, from both the lending and applicant side, so we chatted with them about the major pain points. Here’s a rundown of the most common reasons for rejection, and what you can do to access the funding your business needs.

1. You Haven’t Been in Business Long Enough

Small business loans can be especially difficult for start-ups that need funding to scale. It’s generally recommended that you have at least three months worth of financial records to share when applying for a loan. According to Hometap’s Senior Sales and Marketing Operations Manager, Olin Nelson, who previously owned a small coffee business, it often takes more than that.

“You really need at least two years of profit and loss documentation, so lenders can get a good picture of your revenue over an extended period of time,” he explained.

Hometap Investment Manager Bryan Barry agrees; during his time in the lending space, one of the biggest reasons he saw applications get rejected was that the applicant had only been in business for a short time.

“Less than three years in business was a cause for rejection,” he shared, adding that it was common for applicants to be rejected from multiple lenders as well. “I’d see business owners who had been rejected three or four times before coming to us,” he said, underscoring the difficulty of clearing these application hurdles. While this is partially related to credit score (as we’ll get into below) your business’ credit or profit history may be too limited for lenders to feel confident, even if your score is strong.

2. You Have Bad (Or Limited) Credit

One of the most common causes for application rejection is a low credit score (this all depends on the specific lender, but 640–680 is a good minimum to aim for). However, you can also run into issues if your credit history — whether personal or business — isn’t extensive enough, as demonstrated above. If you’ve recently declared bankruptcy, this decreases your likelihood of being approved as well. Nelson also warns against buying into advice that glorifies ‘bootstrapping’ — or relying completely on your own personal credit and money to get started.

“A lot of small business resources encourage people to keep financing in-house, open credit cards to get started, and buy initial inventory that way, but this can really hurt your prospects for getting funding,” he explained. “Your debt-to-income ratio is going to increase, and that can have a negative impact when you go and try to get a traditional loan after that.”

3. You Have a Low Capacity for Repayment

If a lender believes that you may not be able to repay your loan for any reason, they may deny your application. This can happen if you’ve already taken out another loan elsewhere, if you don’t have much (or any) business or personal collateral, or if your business revenue or capital appears insufficient to cover the balance of the loan. Previous financial documentation that shows evidence of positive historical performance, as mentioned above, increases the likelihood that lenders will feel confident about getting their money back.

“You really need some money upfront,” said Nelson. “I was denied for five different loans in my first year of business because my capital needs to scale the business grew much faster than the purchase orders I was getting. When you don’t have consistent income history, and a bank is willing to help, they’ll require 20-30% down on a loan. When you’re trying to quickly scale a business, and reinvesting profits, it’s difficult to save the cash you need to qualify, and lenders won’t cover things like employee salaries or operational capital because they’re not asset-backed or profit-generating.”

4. Your Industry Is “Risky” or Otherwise Ineligible

Lenders tend to be more reluctant to take on businesses that fall into categories that they deem to be higher-risk. These can include restaurants, used car dealerships, racetracks, and casinos. Barry added that in his experience, “some construction companies were risky because it can often take them 30, 60, or 90 days to get paid on projects.” Other ineligible industries are consumer and marketing cooperatives, rare coin and stamp dealers, and nonprofits. There are additional restrictions on religious organizations due to the separation of church and state.

What to Do if Your Small Business Loan is Rejected

Reapply

Once 90 days have passed from the date your SBA loan application was rejected, you can reapply if you feel that you’ve addressed the issue(s) that led to the rejection — fortunately, this should be quite easy to find out, as federal law states that you’re legally entitled to a written letter of explanation for the rejection. Common steps include strengthening your personal and business credit score and ensuring that your company’s financials are in tip-top shape. In cases where you were rejected due to limited time in business, your best bet may be simply to wait at least a few months.

Consider Alternatives to a Small Business Loan

If your SBA loan was denied, another route is to think about alternatives to a small business loan. A home equity investment, like those offered by Hometap, can be an ideal option for small businesses whose SBA loan application was denied or who don’t meet the criteria for approval.

While a traditional small business loan may allow you to get a low rate, it may not be the best choice if you’re looking to get funding quickly; the loan process can take up to three months and require a site inspection and hard credit pull, whereas a Hometap Investment can get you funds in as little as three weeks. In addition, there are more restrictions that come along with an SBA loan in terms of the use of funds: while you might be limited to equipment purchases, building renovations, or furniture and fixtures, a home equity investment allows you to use the money for whatever you’d like without these often rigid requirements.

While a home equity loan may offer another alternative way for entrepreneurs to access funding, many self-employed homeowners find it difficult to get approved due to the lack of a standard W2.

“Hometap would have been a godsend for my business because of the flexibility it offers,” Nelson said. “With a home equity investment, you can fund that next stage of growth, unlock more channels, and have a reserve of capital when opportunity strikes. When you’re a small business that’s having to pay the debt and interest that comes with a traditional loan on top of already razor-thin margins, it can be a huge challenge.”

See how a home equity investment from Hometap compares to an SBA loan in the chart below:

While it might not be the best fit if you need a large amount of capital, a Hometap Investment offers a shorter funding timeline, no monthly payments or interest, and no criteria on how you spend the money.

See if we’re a fit for your small business needs.

YOU SHOULD KNOW

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

Beyond its year-round warm weather, Florida has a little bit of something for every kind of homeowner, from the family-friendly theme parks of Orlando and historic neighborhoods of Tampa to the beachy lifestyle of Miami. As of November 2020, the statewide median home sale price was $305,000, a jump of 14%, and the number of sales was up nearly 23% year over year, reaching 26,406. The approachable cost of living in Florida has people from all over moving to the sunshine state.

In Smaller Cities, An Optimistic Outlook

In the Orlando area, the median home price for single-family homes was $290,000 in October of 2020, an increase of 10% from 2019. The amount of sales saw an even bigger bump of 25% in the same period of time. Somewhat surprisingly, the housing market in this area has stayed relatively unaffected throughout the COVID-19 crisis.

Ali Wolf, chief economist at Zonda, a housing market research firm, explained to MarketWatch that while the region is synonymous with the hard-hit tourism industry, there’s actually a wide variety of employment sectors in Central Florida that allowed residents to continue working and purchasing homes throughout the pandemic.

Tampa is also booming; a recent Redfin study forecasts that the city will be one of the hottest housing markets this year, noting that the area’s housing prices are, on average, much less than those in Miami, with a median of $345,000 versus $520,000 in September 2020, respectively.

The study also names Jacksonville, where the median sold price for a home was $224,000 in November 2020, as a city to watch. Prices here are expected to grow 6.8% this year. Demand isn’t currently as high as it is in other metros in the state, with homes staying on the market for an average of 56 days.

Searching for Space in South Florida

In the Palm Beach area, real estate is on fire despite the pandemic; this is due in large part to an influx of wealthy homebuyers looking for a less urban environment.

“Anyone with money is fleeing New York and coming here,” Guy Clark, an agent with Douglas Elliman Real Estate, told the LA Times.

Nearby Broward County, which includes Fort Lauderdale, has also been experiencing a big boom in housing. The number of single-family homes sold was up nearly 25% in September 2020 from September 2019, and the median sale price reached $425,000, an increase of 15.6%. This has many real estate professionals speculating that this “bubble” is likely to burst at some point soon, and the market has already shown small signs of slowing down.

Inventory remains a problem statewide, too, with many current homeowners staying put during the past year.

“As of the end of November, our statewide inventory of single-family homes was down 41.3 percent compared to a year ago,” Florida Realtors Chief Economist Dr. Brad O’Connor told The Apopka Voice. “Even listings of properties north of a million dollars, where we’ve had more inventory, are down by almost 25 percent.”

For those who were buying homes, it was all about space.

“What I’ve seen is that everybody looking to buy a house was upgrading,” Gianperre Giusti, a real estate agent with the Meza Group in Fort Lauderdale, told the South Florida Sun-Sentinel. “And more importantly, the fact that you could have this space if you were quarantining, so you wouldn’t feel stuck or get cabin fever.”

Condos have remained relatively flat, likely due to wariness about shared common spaces in buildings.

If you’re a Florida homeowner, growing home values mean that you might have an opportunity to make the most of your home’s value by tapping into your growing equity. Whether you’re looking to purchase a second home, cushion your retirement savings, or grow your business, your equity could help — and a Hometap Investment could let you access it debt-free.

Take our five-minute quiz to see if a Hometap Investment might be a fit for you.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.