Our Investment Managers are experts in helping you tap into your home equity, but you may have more in common with them than you think. Learn a little more about your Investment Manager, their life outside of Hometap, and why they love working with homeowners like you

What’s the best part of your job? How does being an Investment Manager at Hometap differ from your past work experiences?

The best part of my job is getting to work with such a diverse population from all over the country. The job role feels similar to previous jobs I’ve had, however, the company culture and the autonomy I’m given to do my work is next level.

Is there a particular homeowner story that really made an impact on you? What is it and why?

I worked with a homeowner who was deep in debt, mostly from high-interest credit cards. She had a lot of equity in her home but was unable to qualify for traditional financing due to a low credit score. She was really nervous the entire process that we were going to decline her, but we were able to invest enough so she could pay off all of the debts. She cried tears of joy when I called her for the final offer and said, “I can breathe again.”

What are your favorite things to do when you’re not working?

I enjoy spending time with my two kids, and everything about living in the Pacific Northwest. We are often camping, kayaking, making music, dancing, snowboarding, or cooking together.

Describe your dream home.

My dream home would be a simple cabin in the woods with high ceilings and lots of windows.

What’s one thing you wish people knew about Hometap?

We operate with integrity, even behind the scenes.

Hometap’s Vice President of Engineering, Moe Khan, sat down with VentureFizz to talk all-things engineering at Hometap: how the team is organized, what kinds of exciting projects are on the horizon, the tech stack we’re working with, and why now is a better time than ever to join the Hometap team.

If you’re a business owner, a grant might be something you’ve primarily associated with non-business initiatives, like art or nonprofit projects. However, government business grants and foundation-sponsored business grants can be an excellent way to get funding for a specific purpose as it relates to your company.

Simply put, a grant is a sum of money that’s given to a business in need or on a mission with a clear social, economic, or research focus. While there are government grants for small businesses issued by local, state, or federal branches — corporations and foundations also offer them.

Grants are usually cause-based, supporting a particular initiative or focus that’s important to the organization, like research and development, minority- or women-owned businesses, etc. There’s no interest attached to the funding, and you aren’t expected to pay it back. While this concept of “free money” might sound too good to be true, it’s not. The only catch? Competition can be fierce, as the organization issuing the grant only has an allotted amount of cash to provide, which is typically either split between a small number of businesses, or given just to one.

There’s no question that grants can be incredibly valuable to small businesses — but as with any financing source, it’s crucial to do your research to determine if it’s the best way for your company to pay for its needs. Here’s everything you need to know before beginning the process of seeking grant funding.

Pros and Cons of Business Grants

There are benefits and drawbacks to grants. In contrast to loans and lines of credit, you aren’t required to pay the grant money back after you receive it. And because the money is awarded to you, there is no interest or monthly fees associated with it. In addition, the funds are usually provided in one lump sum, so you have access to all of it at once — an advantage if there is a particular item or initiative that you’re hoping to cover the costs for.

Receiving a grant can also increase your chances of being approved for another one in the future, since it demonstrates your merit and trustworthiness to other organizations.

However, there are several factors to be aware of if you’re considering small business grants as a means of funding your business. One of the biggest disadvantages associated with grants is the length of time it can take to go through the process. While it depends on the organization, the timeline from application to funding can take as long as a year or more, since grants are evaluated subjectively by either a panel of reviewers or sometimes even individual staff members, especially if you’re dealing with a foundation or nonprofit with only a few employees. So if you’re hoping for fast cash, grants are generally not your best bet.

Another challenge is that unlike most traditional funding options, there can be some stiff competition depending on the grant, since there’s typically an allotted amount of recipients — and in some cases, only one. While you obviously can’t predict whether or not you’ll be selected, the more tailored the grant is to your business or the desired purpose of the funding, the better your chances are.

Finally, as mentioned above, business grants usually have a very defined purpose, and can’t always be used for anything you’d like. You’ll usually be required to put the money toward a designated area, like technology development, and will likely have to explain in the application process exactly how you plan to spend the money.

For businesses seeking a large sum of cash, a grant may not be the best option — or at least, shouldn’t be the only source of financing. The maximum amount you can receive varies by the organization issuing the grant. The Small Business Innovation Research (SBIR) grant, for example, can provide anywhere from $150,000 to $1,000,000. But most (especially those offered by local companies) tend to provide fairly small sums, from $10,000 to $50,000. Considering the drawbacks above, it typically makes the most sense to go the grant route if you’re seeking a relatively small amount of money for a very specific reason and feel that you can confidently demonstrate a clear need that stands out from that of other candidates.

How to Get a Small Business Grant

The application process and qualification criteria vary based on the organization that’s issuing the grant, but corporate grants are typically less stringent than government grants. When it comes to applying, it almost goes without saying that you should first make sure you meet all of the prerequisites — as some organizations have stringent requirements about number of employees or business type — and make sure you provide information that’s as complete and accurate as possible. Thoroughly proofread your submission and double check aspects or requirements that are easy to overlook but can instantly disqualify you, such as word or character count. Here are some other tips to keep in mind that can up your chances of acceptance.

Match the Mission

You should also make sure that your business aligns with the values and mission of the organization you plan on applying to. This will not only increase the likelihood that you’ll be selected as a grant recipient, but also help you to tailor your application to fit the requirements of the sponsor. As mentioned above, businesses that fall into a designated category — like women- or minority-owned, eco-friendly, etc. — often stand the best chance of qualifying for specialized grants, as there tend to be fewer companies that meet the criteria to apply.

Learn from Past Grant Recipients

If possible, another helpful step is to familiarize yourself with previous winners of the grant. Reading about those that were successful in receiving funding from the issuing organization can give you a huge leg up in terms of potentially understanding the values, qualities, and qualifications that may help you stand out from the pack.

Focus on the Facts on Your Grant Application

Including numbers and figures is another great way to provide concrete proof that your business is deserving of the particular grant. For example, if you can show data that supports demand for your product and growth potential, this can illustrate your success in a direct and objective way and make your application that much stronger. If you’re looking for a startup or new business grant and don’t yet have these figures, going broader and citing more general statistics about your industry, like growth rate or market size, can work as well.

Overall, a comprehensive and solid business plan can distinguish your company from the pack and better explain your needs. Now is also a good time to tout any awards or accomplishments you’ve won in the past; don’t be afraid to share examples of positive recognition that can convince the committee that your company has an established, positive track record.

Share Your Business’s Story

Don’t underestimate the power of telling the story of your business if it can strike an emotional chord with the organization or provide a compelling reason why the grant could make a difference for you, either. Some questions to consider as you craft your submission are:

Why did I start this business?

What kind of difference was I hoping to make or problem was I hoping to solve with my product or service?

Is there a particular event that happened or a challenge that I overcame that illustrates a particularly important aspect of my journey so far?

Plan Ahead

If there’s a recommendation component (which many grant applications require), it’s best to reach out to your contacts as far in advance of the deadline as possible so you aren’t stuck waiting for those endorsements to complete your submission. The same goes for any public or customer voting programs, which are an element of some applications; you’ll want to plan ahead to determine how and how often to encourage your customers to cast votes — like through a social media post on a daily basis, for example.

Address Any Shortcomings

While you obviously don’t want to discuss the weaknesses of your business in depth, it can certainly help to get ahead of any potential questions that the organization might have about an aspect of your business that could require more explanation, like your business model, for example, if it’s complex or potentially confusing. Being as thorough and honest as possible can paint you in a more favorable light to the judging panel.

Leverage Your Connections

It may also help to acquaint yourself with the particular organization’s grant officer to build a relationship and gain insight into what they might be looking for from an applicant. Finally, while it’s not necessary for every business, it can be beneficial to bring in an outside expert — like a consultant or accountant — to advise during the process and review your application before you submit it to increase your chances of success. If you plan on applying for multiple grants, consider hiring a dedicated grant writer, who is experienced in crafting these kinds of applications. However, taking the time to research all of the potential grants available and selecting one or two that you feel you’ll have the best chance of winning can often be a better use of both your company’s time and money.

Even after you submit your grant application, it may be worth the effort to follow up with the organization once or twice, especially if the review period is lengthy. With so many submissions to sort through, this can go a long way to keep you top of mind and in good standing with those who are evaluating the applications.

Where to Find Business Grant Opportunities

If you’re looking for a grant, there are plenty of places to find options that may be right for you. While it primarily depends on the type you’re looking for, a good place to discover federal grants is grants.gov, which is a large, searchable database of opportunities, categorized by organization. The Small Business Administration website also has a handful of SBA grant programs listed that can help you narrow your search. While there are not SBA grants for starting or expanding a business, there are grants for nonprofits, resource partners, and educational organizations that support entrepreneurship.

For regional or local grants, your state’s official web page will likely have a section for opportunities you can pursue. Of course, your own industry may have dedicated grants as well, so it’s worth a quick search for your particular field.

To get started with finding the best grants for your organization, here is a list of some specialized resources that may help you identify appropriate opportunities:

Visa Everywhere Initiative: Expressly geared toward startups who are creating solutions in the commerce and payment spaces and open to companies around the world.

The Amber Grant Foundation: Women-owned businesses have the chance to receive $10,000 each month — and $25,000 in the month of December — through The Amber Grant Foundation.

Black Founder Startup Grant: If you have a legally registered business and identify as a Black woman or Black nonbinary person who is seeking investor funding for your company, you can apply to receive between $5,000 and $10,000 from the SoGal Foundation and its partners.

U.S. Department of Energy (DOE) Grants: The U.S. Department of Energy gives grants to small businesses that are doing work in the fields of clean energy research and development.

The Military Challenge Award:Veterans, reservists and transitioning active duty military members (or their spouses) whose businesses have a social mission for the military community can participate in this pitch contest, sponsored by the Street Shares Foundation.

Walmart Local Community Grants: This program, sponsored by Walmart, is specifically for community-focused non-profits, and provides $250 to $5,000 to selected recipients.

Nike Community Impact Fund: This partnership between Nike and the Charities Aid Foundation of America, gives grant money to urban nonprofits that serve their communities through sports programs.

National Institute of Health (NIH) Grants: For small businesses with a focus on biomedical or behavioral research, the National Institute of Health has thousands of grant opportunities listed on their website.

Economic Development Administration (EDA): Regional and national economic development projects can receive funding for projects from the EDA, a subset of the Department of Commerce.

Free business funding is free business funding, so small business grants are a worthwhile option to pursue. However, due to the stiff competition and often lengthy funding timeline, if you need additional business funding, grants shouldn’t be your only plan. If you’re looking for alternative funding beyond small business loans, perhaps because you haven’t been in business long enough to qualify, you do have more options. If you’re a homeowner, your home equity could provide the extra funding you need to launch or scale. Here are four ways to access that equity.

Home Equity Loan for Business Funding

A popular option for many homeowners, a home equity loan lets you borrow against the equity in your home — with the home serving as collateral. One advantage is that your monthly payment will stay consistent every month due to fixed interest rates. Plus, repayment periods range from 5 to 30 years, giving you time to pay the money back, and the interest that accrues on your equity may be tax deductible. But it’s important to remember that a home equity loan is a second mortgage on your home, so you’ll be responsible for another payment every month beyond that for your original mortgage. Finally, while application and approval requirements differ by lender, some can be quite stringent and restrictive, making the process difficult.

Home Equity Line of Credit (HELOC)

A HELOC can be fantastic in terms of flexibility for your business, because it gives you access to your home equity in the form of a credit line from which you can borrow as much money (up to a maximum) as often as you want without being penalized. Like home equity loans, the repayment periods are typically flexible, ranging from 15 to 20 years. However, HELOCs usually have variable interest rates, so your payments have the potential to fluctuate every month, which can be a disadvantage if you want the peace of mind that comes with predictability. You also run the risk of having the credit line frozen by the lender if your score or home value drops too low.

Cash-out Refinance

A cash-out refinance replaces your original mortgage with one with a balance larger than what you owed, giving you the difference. There are advantages to this option, including the opportunity to secure a lower interest rate on your mortgage. But it’s important to remember that since it is a new mortgage, your payoff timeline will be extended and you’ll have to pay application, closing, origination, and potentially appraisal fees.

Home Equity Investment for Business Funding

There’s an alternative option to a business grant that also gives you money in a lump sum, can provide you with cash in as little as three weeks, and allows you to use the money however you choose — without the fierce competition and uncertainty that can come with the grant application and selection process. A Hometap Investment lets you tap into your home equity to get cash in exchange for a share of your home’s future value, without interest or monthly payments.

See if a Hometap Investment might make sense for your business needs. Take our five-minute quiz and find out today.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

Our Investment Managers are experts in helping you tap into your home equity, but you may have more in common with them than you think. Learn a little more about your Investment Manager, their life outside of Hometap, and why they love working with homeowners like you.

What’s the best part of your job? How does being an Investment Manager at Hometap differ from your past work experiences?

Our homeowners are definitely the best part of my job! I love that we can help them accomplish any goal they have!

Is there a particular homeowner story that really made an impact on you? What is it and why?

There are so many homeowners we have helped in the past that I still think about today. One in particular was a woman who was using some of her Investment to help her granddaughter receive a life-saving medical treatment. I was so honored to be a small part of that incredible experience.

What are your favorite things to do when you’re not working?

In my free time, I love spending time with my husband and our two kids. We enjoy traveling, cooking, and visiting our families.

Describe your dream home.

A six-bedroom, modern white farmhouse on 50 acres in my hometown.

What’s one thing you wish people knew about Hometap?

We are so different from debt-based home equity products that have been around for ages and we truly care about every single one of our homeowners.

Our Investment Managers are experts in helping you tap into your home equity, but you may have more in common with them than you think. Learn a little more about your Investment Manager, their life outside of Hometap, and why they love working with homeowners like you.

What’s the best part of your job? How does being an Investment Manager at Hometap differ from your past work experiences?

The best part of my job is being able to help homeowners. With this job, I know I am able to make a difference in people’s lives.

Is there a particular homeowner story that really made an impact on you? What is it and why?

Yes, I worked with a homeowner who lost his job due to COVID and was not sure how he’d be able to pay bills and maintain it while searching for a new job in these crazy times. Knowing that a Hometap Investment is something that could ease his mind and allow him to focus without having to stress about being able to pay his bills on time was refreshing.

What are your favorite things to do when you’re not working?

I enjoy traveling, going to sporting events, and being with family and friends.

What’s one thing you wish people knew about Hometap?

That we are dedicated to helping homeowners achieve their goals.

Working for yourself can be fantastic for a number of reasons — but when tax time comes around, things can get tricky because unlike employees who receive W-2s, taxes aren’t automatically deducted from your paychecks when you’re self-employed. While you should consult a tax advisor for the specifics, here are some things to consider as tax season gets underway.

How do you know if you’re technically self-employed or not? The IRS classifies self-employment through the following criteria:

You carry on a trade or business as a sole proprietor or an independent contractor.

You are a member of a partnership that carries on a trade business.

You are otherwise in business for yourself (including a part-time business).

The window to file your taxes in 2022 extends from January 24 to April 18 for all taxpayers, whether self-employed or not. However, there are some important differences between filing taxes as a self-employed individual and a company-employed individual that you should be aware of before you begin the process.

Key Differences for Self-employed Taxpayers

You’ll likely need to file an income tax return if your net earnings from self-employment were at least $400. You’ll also be required to pay a self-employment tax in addition to income tax. The self-employment tax rate is 15.3%. It’s important to note that this percentage breaks down into two elements: the social security tax (12.4%) and the Medicare tax (2.9%).

Before you file, you’ll also need to determine your specific tax rate, and whether your area has specific city taxes you’ll need to pay. To figure out your tax rate, you’ll first need to find your net profit or net loss from your business by subtracting qualified expenses from your income.

In order to file taxes when you’re self-employed, you’ll need to have a social security number (SSN) or, if you are a nonresident or resident alien, an individual tax identification number (ITIN). For certain types of businesses, you may need a tax ID number (also known as an Employer Identification Number). It’s free and easy to obtain one.

If you operate your business as a sole proprietor, you’ll need to use the Schedule C (Form 1040) to report your income and expenses and file your annual tax return.

Ways to Save Money When Filing Taxes If You’re Self-employed

A tax deduction is only able to lower your taxable income, as well as the tax rate that is used to calculate your tax, and this can lead to a more significant refund on your withholding.

A tax credit, on the other hand, actually decreases the amount of tax that you owe. So while you’ll also receive a larger refund on your withholding, you may also receive a refund without a withholding, depending on the particular credit.

These are some common deductions:

If you recently started your own business, you may be able to deduct the startup expenses, like legal and marketing costs, from your tax bill. You can expect to deduct up to $5,000 in business startup costs and up to $5,000 in organizational costs, but only if your total startup costs are $50,000 or less. Start-up costs don’t include deductible interest, taxes, or research and experimental costs.

If you use a vehicle to travel for specific job-related purposes, you may be able to deduct up to $25,000 in costs, plus mileage expenses.

If you have a dedicated home office, you may be able to deduct rent/mortgage, property tax, and utility costs based on square footage.

If you use any specific supplies or equipment that are critical to your job functions, you might be able to deduct their costs.

Even though you’re required to pay the full Social Security and Medicare tax, you may be able to write off half of this amount at the end of the year.

If you pay health insurance premiums, you may be able to deduct these costs.

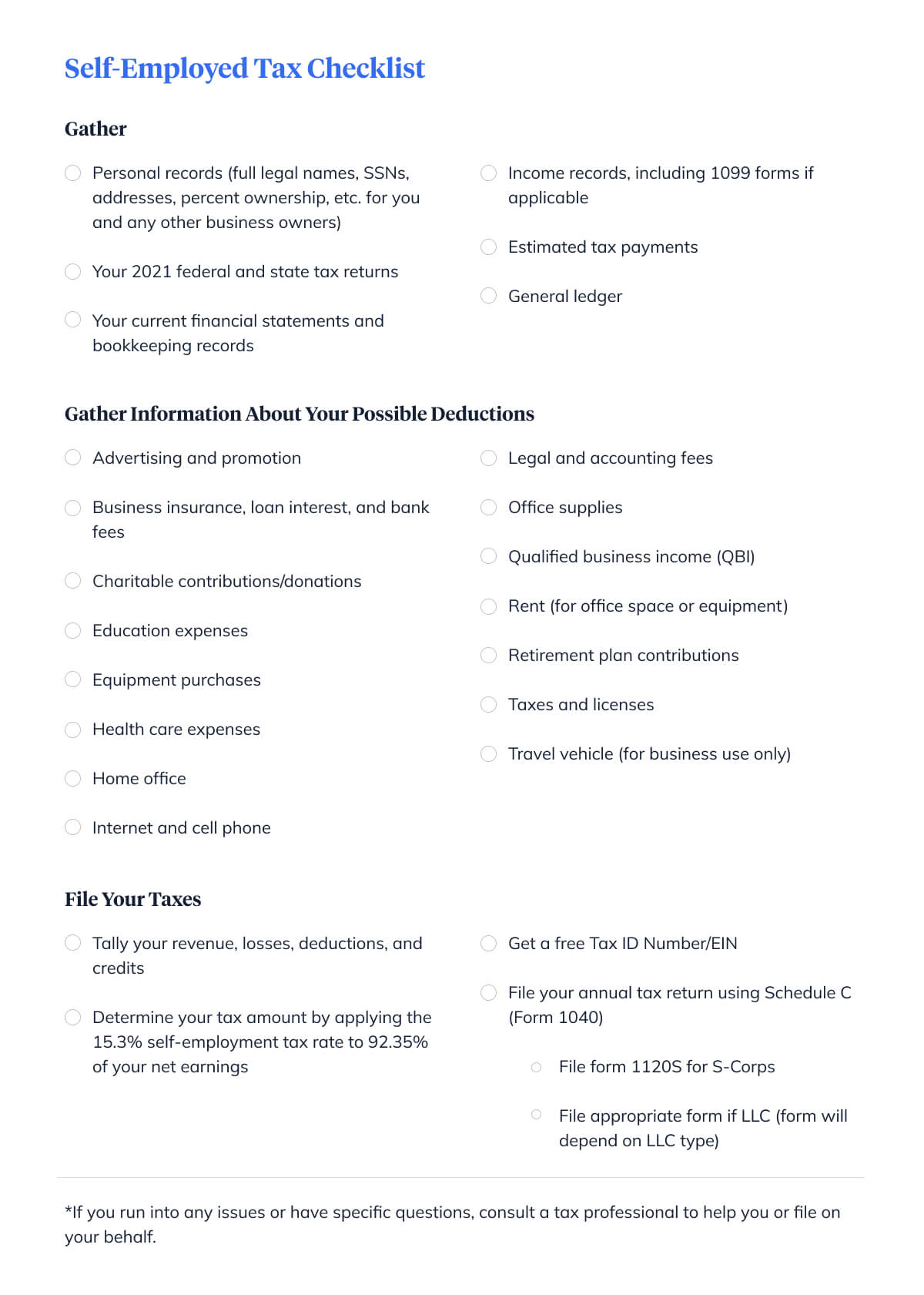

Self-employed Tax Checklist

Here’s a quick checklist to help you prepare to file your taxes for the first time as a self-employed individual. (Here’s a free, print-friendly version of the tax checklist, too).

Gather these items:

Personal records (full legal names, SSNs, addresses, percent ownership, etc. for you and any other business owners)

Your 2021 federal and state tax returns

Your current financial statements and bookkeeping records

Income records, including 1099 forms if applicable

Estimated tax payments

General ledger

Gather information about your possible deductions:

If you run into any issues or have specific questions, consult a tax professional to help you or file on your behalf.

If you’re a self-employed homeowner and you owe more than you expected in taxes this year, your home equity might be able to help you handle the cost without taking on more debt. A home equity investment can provide you cash in as little as three weeks, with no interest and no monthly payments, and doesn’t require a W2 to qualify.

Request an estimate to see how much of your home equity you could access in just a few minutes.

YOU SHOULD KNOW

The information above is intended as a basic summary of some tax issues to think about as a self-employed individual. It is not intended to be tax advice, as everyone’s tax circumstances are unique. If you are self-employed and have questions about your taxes, seek help from a tax professional.

If you’re a business owner who collects payments from customers through invoicing and is looking to free up a significant amount of cash without having to take out a loan, both invoice financing and invoice factoring can be great options for you. However, it’s important to first understand the differences between the two, as well as the pros and cons of each, and additional financing choices to consider before you decide to go with one or the other.

What Is Invoice Factoring?

Invoice factoring is an alternative to a loan that allows you to sell your invoices at a discounted price to a designated factoring company and receive a lump sum of cash in return (typically 80–90% of the invoice totals) minus a fee set by the company. Once your customers pay the invoice factoring company — which usually takes anywhere from 30 to 90 days — you’ll receive the rest of the invoice amount from the company, most commonly as a direct deposit into your bank account. The seamless process makes it fairly quick and simple to begin using the money for working capital in a relatively short period of time.

What Is Invoice Financing?

Invoice financing differs quite drastically from invoice factoring in that you’re not selling the invoices like you are with invoice factoring, and you’ll still be dealing directly with your customers. You’re receiving what is essentially a short-term loan from a lender and pay a percentage of the invoice amount as a fee for borrowing the money.

This option, also known as accounts receivable financing, can be a better choice for your business if you’re concerned about the potential ramifications of shifting the responsibility of invoice collection to an outside company and/or don’t want your customers to have to deal with an outside vendor, especially if your business relies on building and maintaining a relationship with clients.

Pros and Cons of Invoice Financing and Factoring

The primary advantage of both invoice factoring and financing is that they allow business owners to maintain cash flow, handle the payment of bills, and pay out their employees quickly, without the need to wait for outstanding client invoices to be dealt with first. This is often a step that can cause frustration and delay for many companies that frequently find themselves waiting for clients to settle their balances. The application and approval processes are often quicker and easier than that of a loan as well, typically just requiring a credit check to verify that your business is financially stable. Along with an application-to-funding timeline of around one to three months, they can be fairly quick ways to access cash compared to other financing methods that have lots of red tape and stringent qualification criteria.

In addition, factoring and financing are considered “unsecured,” so it doesn’t require any collateral to guarantee the funding beyond the invoices.

The biggest con of using either of these funding sources is the cost, as they can be quite expensive compared to other financing choices. Since you’re paying a premium to have the money given to you, and the financer is taking on risk by attempting to collect from your customers or provide you with the cash up front, you won’t receive the full sum of the invoices and they’ll receive a cut of the total. In addition, you may need to end up buying back the invoices that aren’t collected or agree to a recourse situation. Depending on the company you go through, extra fees usually range from 1-5%, but for financing providers who bill per total invoice value per week, this can balloon into massive APRs of nearly 80%, so it pays to do your homework on the specific lender.

With invoice factoring specifically, you’ll also need to be comfortable relinquishing control over your invoices and involving a third party — once you sell your invoices to them, your customer will need to work directly with that company to handle the payment of their invoice. Depending on your industry and the nature of your relationship with your customers, this can potentially have a negative effect on your future interactions.

Of course, your business also needs to collect invoices from vendors or clients for factoring to be a viable choice; if you rely on a different method for payment, you won’t be able to consider this option.

Who Offers Invoice Financing and Factoring?

For invoice factoring, you’ll need to work with a specialty factoring company, as this service isn’t offered by traditional finance providers. Similarly, invoice financing is typically not available through banks and credit unions — but some online lenders and fintech companies provide it.

Alternatives to Invoice Financing and Factoring

If you’re a homeowner who doesn’t feel like invoice factoring or financing is right for you or you’re having a hard time finding a company that’s a fit, there are more than a few other ways to access cash for your business, specifically through your home equity.

Home equity loan alternative

With a home equity loan, you borrow against the equity you’ve built in your home with the house serving as a guarantee on the loan. Unlike a business line of credit, you aren’t required to pay the balance down to zero every year. There are several other advantages to this option, including a fixed interest rate, consistent monthly payment, and flexible repayment period that typically ranges from 5 to 15 years. There are downsides to be aware of, however. Since a home equity loan is another mortgage on your home, it means another payment you’ll need to make each month on top of your first mortgage. And depending on the specific requirements of your lender, the application and approval process can be quite lengthy and challenging.

Home equity line of credit (HELOC) alternative

A HELOC lets you access funds whenever you’d like, and you can take out as much as you want — up to the maximum amount you qualify for — without any penalties. Compared to a loan, application and approval might be a bit easier, and repayment timelines are usually between 15 and 20 years. On the other hand, HELOCs have variable (read: unpredictable) interest rates, so your monthly payment can fluctuate significantly. You also run the risk of having your line of credit frozen by the lender if your credit score or home value drops below a certain threshold.

Cash-out refinance alternative

A cash-out refinance essentially replaces your current mortgage with one that has a larger balance than what you owed and provides you with the difference. While you have the opportunity to lock in a lower interest rate with a refinance, you are paying off a new mortgage, so this option lengthens your timeline and you’ll run into the same fees you dealt with the first time around.

Home equity investment vs. invoice financing

A home equity investment lets you access the equity you’ve built in your home and gives you cash in exchange for a share of the home’s future value. You can get the money in as little as three weeks and use it toward whatever your business needs, without the hassle of interest or monthly payments.

Take our five-minute quiz to find out if a Hometap Investment might be a good fit for your business as an alternative to invoice financing or factoring.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

If you own a business, you already know the importance of maintaining your cash flow no matter what stage your business is in. Understanding all of your funding options is crucial, so that when your business requires an influx of cash, you can make the best decision possible. Below, we’ll cover everything you need to know about business lines of credit and how they work.

A business line of credit provides a business with funding that can be used for any expense they choose, from equipment purchases to office space. While they may seem less common than loans or credit cards, according to FitSmallBusiness, nearly half (47%) of small businesses have opened a line of credit.

What’s the Difference Between a Business Line of Credit and a Business Credit Card?

While business lines of credit and business credit cards are similar, they aren’t the same. With a line of credit, you have a draw period, or a specific number of years that you can tap into the funds. A business credit card, like a line of credit, has a maximum limit, but does not have a draw period, so you can maintain your account for as long as you’d like.

However, unlike a business credit card, a business line of credit is revolving. This means that you can use the funds up to the approved limit and, once you pay it off, you’re able to begin taking out money again. Some lenders charge a draw fee each time you access the credit line, and while APRs can be high, you only pay interest on the funds you use — this is a huge plus and can save you quite a bit in interest compared to other financing methods like a loan.

In addition, the repayment schedule varies by lender, but is typically weekly or monthly. Business lines of credit are offered through many traditional financial institutions like banks and credit unions, but are also available through some online lenders. Many business lines of credit limits are also higher than those of credit cards, which can be an advantage if you’re seeking funding for a larger expense. A business line of credit can also cover expenses that might not be as easy to charge on a credit card, like rent or payroll costs.

This option also differs from a personal line of credit in that it’s connected to your company rather than you as an individual. This can be a positive or negative depending on how long your business has been running and your financial history, as you’ll need to show proof of strong revenue and business credit history in many cases, which is often tough for businesses that are just getting started.

There are two types of credit lines: secured and unsecured (sometimes referred to as non-secured). A secured credit line requires collateral — like a home — to guarantee it, whereas an unsecured line does not. While the approval criteria for unsecured lines of credit may be more stringent since it’s a riskier proposition for the lender, most business owners prefer this option for the obvious reason that there are no assets at stake. If you end up defaulting on a secured line of credit or are delinquent on your payments after a period of time specified by your lender, they may take ownership of the collateral and liquidate it to handle the balance owed.

How Much Money Can I Access and How Do I Qualify for a Business Line of Credit?

To determine how much money you may be able to access for your business through a line of credit, you can start by taking your estimated annual gross revenue and divide it by 365 to figure out your daily cash need. Then, total your number of accounts receivable and inventory days on hand, and subtract your accounts payable days on hand to get your usage. Finally, multiply this number by your daily cash need to get an estimated line of credit maximum.

While requirements differ by lender, you usually need to be in business for at least six months, have at least $25,000 in annual revenue, and have a minimum business credit score of 500 to qualify. You’ll also need to provide documentation that may include financial statements like balance sheets and tax returns.

Pros and Cons of a Business Line of Credit

Business lines of credit come with both pros and cons, like any financing option.

Pros

Flexibility: One big advantage is that you have quite a bit of flexibility in terms of access and use: a line of credit is revolving, meaning that once you access the maximum amount you’ve qualified for and repay it, you’re able to begin taking out money again right away. And unlike traditional financing options like a loan, you don’t necessarily have to specify what you plan to put the funding toward when you apply for a line of credit.

Cash Flow Maintenance: A business line of credit can also help you maintain a healthy cash flow and timely payment of your bills, especially if you opt for automatic payments, which can lead to discounts from the lender. With the ability to take out as much money as you want up to the maximum amount, as often as you’d like, it helps you avoid the risks of overspending with a lump sum. This can be more advantageous than receiving a single payment for some companies as well, especially if your needs are spread out over a longer period of time. For example, if you’re planning a lengthy construction or renovation project where you’ll need more infusions of cash at different points, a line of credit might make more sense than a one-time loan.

Future Financing Needs: A business line of credit can be a good way to grow and build a solid credit history for future financing needs as well, as many lenders require substantial financial records and credit history in order to approve you for loans and refinances. If you’re careful and responsible with it, the line of credit could actually help you increase your business credit score over time. And if you repay the amount you owe before the end of your draw period, you most likely won’t have to deal with any fees or penalties.

Cons

Costs: The biggest con of business lines of credit is that they can be quite expensive, with APRs as high as 10-20%, plus other fees. These can vary widely by lender, so it can pay off (literally) to thoroughly research your options before choosing one. If it’s an unsecured line of credit, it will likely have a variable interest rate, which means monthly payments can change unpredictably month to month.

Challenging application process: The application process for a line of credit tends to be quite restrictive and demanding, with a typical credit score requirement of 600 at minimum — though it’s recommended that you shoot for an even higher score to increase your chances of approval.

Potential for quick debt accumulation: You have the potential to go into debt more quickly with a business line of credit than other funding sources, as the interest will compound onto the new principal amount if you miss even one monthly payment. The flexibility to take out as much cash as you want can also lead to trouble when you don’t keep an eye on your spending.In extreme cases, if you’ve ended up using the entire amount you qualified for and run into an unexpectedly slow period of low cash flow, you might find yourself unable to pay back the money — so it’s critical to first consider why you’re seeking funding and whether a one-time lump sum payment would be a better match.

With an unsecured line of credit, it’s also recommended that you pay down your balance to zero several times during your term, which can be a hassle for some businesses. Business lines of credit are often a good choice if you are seeking a short-term financing solution — for example, you need to pay for a new piece of equipment, buying extra inventory in anticipation of a busy sales period, or hiring additional employees as you scale rapidly. Given the high fees and risks of debt that come along with business credit lines, it may not necessarily be a great fit if you are looking for a long-term and consistent funding source, simply because of the variable interest rates and potential for missed payments to add up quickly.

Who Offers Business Lines of Credit?

You can find business lines of credit through most traditional financing providers, like banks and credit unions. However, they can have very specific minimum requirements and rigid qualification criteria, so it may be worth exploring offerings from alternative online lenders, whose processes may be faster and less restrictive. While it depends on the specific provider, banks generally want to see at least three years of revenue and strong financial records in order to qualify applicants. On the other hand, while online lenders may be more lenient, their fees can be much higher than those of traditional financial institutions and the repayment periods tend to be shorter, from 6 to 24 months.

If you don’t think a business line of credit makes sense for your funding needs, there are other financing avenues to consider as well, many of which involve using your home equity toward your business. While it does add some level of personal liability, it can often be easier to qualify for a personal line of credit, especially if your company is fairly new and doesn’t have a substantial track record in terms of statements and credit history that most lenders require.

Home equity loan

With a home equity loan, you’re using your home as collateral and borrowing against the equity you’ve built up in your home. There’s a flexible repayment period that ranges from 5 to 30 years, and unlike a line of credit, it doesn’t matter whether or not you pay the balance down to zero every year. But while these loans have fixed interest rates and predictable, consistent monthly payments (a plus for business owners), you are taking on a second mortgage with this option, meaning you’ll have another monthly payment to worry about. The application and approval process can prove difficult depending on lenders’ specific requirements, too.

Home equity line of credit (HELOC)

Similar to a business line of credit but using your home equity as a source of cash, a HELOC can also give you on-demand access to cash. The application and approval processes are often less restrictive than those of a loan, but like a loan, the interest that you pay on the money may be tax deductible. Repayment terms are fairly long, ranging from 15 to 20 years.

But also just like a business line of credit, home equity lines of credit have variable interest rates which means that your payments may fluctuate drastically every month. Your lender also has the ability to freeze your HELOC at any time if your credit score or home value drops too low.

Cash-out refinance

A cash-out refinance — which replaces your original mortgage with one that has a larger balance than what you owe and gives you the difference in cash — can provide you with funding for your business, and it can also help you to lock in a lower interest rate on your mortgage. However, because you’re basically paying off your previous mortgage with your current one, your timeline will be lengthened and you’ll have to pay application, closing, origination, and possibly even appraisal fees.

Home equity investment

A home equity investment gives you cash in exchange for a share of your home’s future value. There’s no interest or monthly payments to worry about, and like a line of credit, you’re free to use the money as you wish for anything your business needs: equipment and supplies, marketing, hiring, or office space. Plus, this option lets you maintain critical cash flow to keep your company running smoothly. You have 10 years to settle the Investment through a refinance, buyout with savings, home sale, or loan, and there aren’t any fees or penalties for settling the Investment early.

If you’re looking for a funding option for your business that doesn’t come along with the stress of interest or monthly payments, a Hometap Investment might make sense. Take our five-minute quiz to see if a Hometap Investment could be a fit for your business financing needs.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

With a high homeownership rate of 70% and an overall cost of living that’s less than the national average, it’s no question why many choose to make the Great Lakes State their home. As of November 2021, the average home value in Michigan was $218,419, a 16.7% jump year-over-year. The market here is hot — and has been for a while.

Rising Prices and Dwindling Inventory

According to the S&P CoreLogic Case-Shiller Index, in the metropolitan Detroit area in August 2021, home prices were 144% higher than the lowest values during the Great Recession of 2007–2009.

And like many other areas of the country, the region and state are facing issues of low supply and high demand. In October, on-market listings were down 13% from the same time in 2020.

“We don’t have enough homes being built, we don’t have enough existing homes,” Jeannette Schneider, president of RE/MAX of Southeastern Michigan, told Click On Detroit. “Until that changes … the rest of this year and even into next year, I don’t see it changing dramatically.”

On the bright side, the market in this area has calmed down ever so slightly since the summertime. “What I have seen is that the frenzy that I saw — buyers were crazy for houses — has cooled a little bit,” Schneider said. “(We’re seeing) five or six offers, not 20 offers.”

Survey Reveals Financial Savviness Among Michigan Homeowners

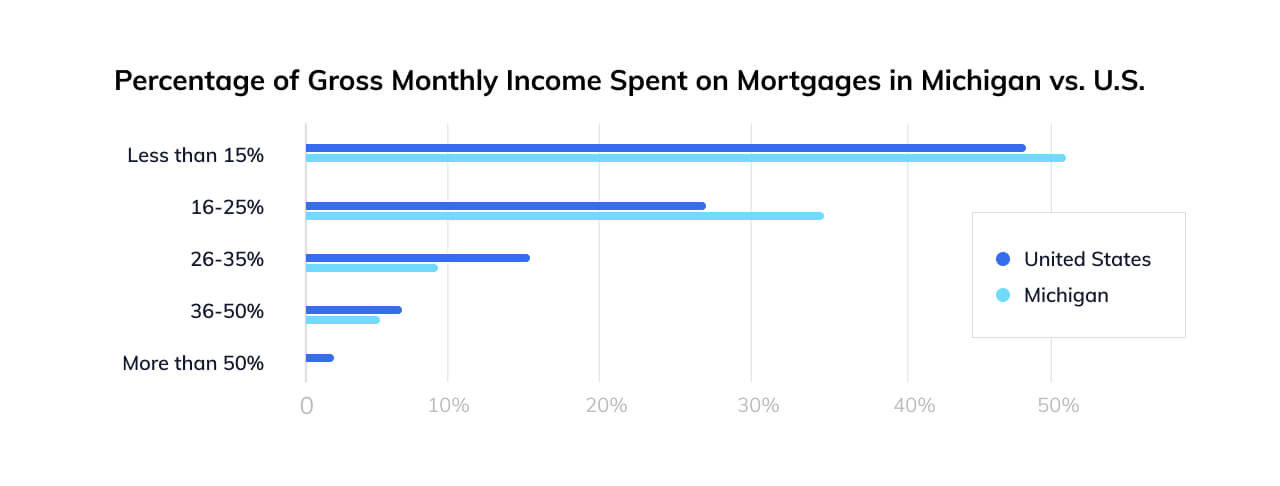

Current homeowners in the state, though, seem to be in an advantageous position at the moment. According to the results of Hometap’s 2021 Homeowner Survey, a significant amount of Michigan homeowners reported having no debt (31.7% vs. 22.7% nationally). Monthly spending remains fairly low among this group as well, with 90.2% spending less than 15% of their gross monthly income on homeownership costs like repairs, taxes, and insurance.

It’s not surprising, then, that Michigan also had the lowest percentage of homeowners who felt that they needed to recover financially from the pandemic (31.7% compared to 42.8% nationally). And all of those surveyed in the state who did have debt were somewhat or very aware of how much they owed, with none reporting that they were unsure or didn’t know how much they had.

The state’s homeowners have a number of financial goals, but the largest ones are practical: growing their retirement savings (43.9%) and paying off credit card debt (41.5%).

…And Untapped Opportunities, Too

Still, Michigan homeowners reported being less ready for the costs of homeownership overall than those in other states, with 22% of those surveyed feeling not very prepared — or not prepared at all — compared to 16.6% nationally.

Despite this, 61% of those surveyed in Michigan considered their home to be an asset, versus 48% nationally. However, nearly half of respondents from the state (48.8%) don’t know how much equity they have in their home — and of those, 45% said that they didn’t feel that they needed to know in comparison to 30% nationally. 35% answered that they did not know how to calculate it, compared to the 47.2% national average.

Of those who said they didn’t see their home as an asset, half reported that it’s because they have simply never considered it as an option through which to access cash.

While homeowners in Michigan generally recognize the opportunity that their home may present and the majority likely know how to determine how much equity they have, our survey reveals that there’s still a knowledge gap for many when it comes to viewing their homes as a way to fund life expenses and reach their financial goals.

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.