Our Investment Managers are experts in helping you tap into your home equity, but you may have more in common with them than you think. Learn a little more about your Investment Manager, their life outside of Hometap, and why they love working with homeowners like you.

What’s the best part of your job? How does being an Investment Manager at Hometap differ from your past work experiences?

Being able to connect great homeowners with a great solution that can help them reach their goals! The entire Hometap team is very customer-centric and it drives our results everyday!

Is there a particular homeowner story that really made an impact on you? What is it and why?

Being able to help a veteran fund his business and help him get current on his mortgage before starting his next deployment!

What are your favorite things to do when you’re not working?

Explore the beaches in Florida!

What’s one thing you wish people knew about Hometap?

That the product allows the home to pay for itself in a sense.

While rising home prices and interest rates have presented major challenges for prospective homebuyers, homeowners in many parts of the country are sitting on record-high amounts of equity. In Q1 of 2022 alone, equity jumped 32.2% and national homeowner equity grew $3.8 trillion — with the average homeowner gaining $64,000. While there are a few different factors at play, including those skyrocketing home prices, low inventory, and a surge of renovations and remodels spurred by the pandemic, the end result is a whole lot of equity for a whole lot of people.

Here are the 10 states where homeowners have gained the most equity this year.

The average California homeowner has gained $141,000 year over year from the first quarter of 2021. California also has some of the highest home values in the entire country, with a median home price of $799,311 — an 18.5% jump between June 2021 and June 2022.

Homeowners in Hawaii gained $139,000 in equity on average between 2021 and 2022. Hawaii is also known for its high home values, with the typical price coming in at $901,942. Home prices shot up 22.1% year over year between June 2021 and June 2022.

In Washington, the average homeowner’s equity grew $114,000 in 2022. The typical home value here is $627,555, a 21.2% increase year over year from June 2021 to June 2022.

Arizona homeowners earned an average of $96,000 in equity from Q1 2021 to Q1 2022. And while the typical home value in Arizona — $450,629 — is significantly lower than states like California and Hawaii, prices have surged 26.3% in one year. Arizona homeowner David was able to use his equity to fund an investment property with a Hometap Investment. Read how he did it.

Colorado

Homeowners in Colorado experienced a $92,000 average equity increase this year. Here, the typical home value is $591,189, and prices have surged 21% from June 2021 to June 2022.

More than ever, homeowners have the opportunity today to tap into their equity to reach their financial goals — from paying down debt to making much-needed renovations or funding an education.

Are you a homeowner who wants to make the most of your equity? Take our five-minute quiz to see if a Hometap Investment might be a fit for you.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

When it comes to retirement planning for women, some of the current stats may surprise you. Nearly one third of adult women (29%) don’t have a retirement strategy in place. The figures around what percentage of women invest in their retirement are similar: the Teachers Insurance and Annuity Association (TIAA) recently found that just 31% of those surveyed are saving for retirement, as opposed to 44% of men. This information is especially concerning, considering that women live longer than men on average, typically earn less than men during the span of their career, and receive fewer retirement benefits on the whole than men as well.

But If you’re a woman who has yet to start saving for retirement, it’s not too late. While it can seem overwhelming to know where to start, taking it step by step can make the process much more manageable and less stressful.

Enlist the Help of a Financial Planner

Experts recommend first meeting with a financial advisor. If your employer provides a retirement plan like a 401(k), you can likely connect with that company, and they can refer you to an in-house planner who can begin working with you to establish retirement goals and help you make strides toward reaching them.

Decide on Your Approach

There are a few different schools of thought when it comes to determining the amount of money you’ll need to retire. Here are the most common ones:

Strategy #1: The End Result

This approach holds that you should save 10 to 12 times your annual income by retirement age. While this is wise, you’ll want to make sure you have some more granular milestones in place to keep yourself on track (see below).

Strategy #2: Pace Yourself

A pacing plan takes the above idea a little further, advising that your savings should be equivalent to a multiple of your annual income as you age. For example, by age 30, you should have set aside as much as you’re making per year. By age 40, your retirement fund should be equal to three times your salary, six times by age 50, and so on — leading to 10–12 times your salary by age 67.

Strategy #3: Percentage Plan

Similar to strategy #1, this approach advises that you should have saved enough money to replace 60–100% of your pre-retirement annual income by the time you retire.

Strategy #4: Who Wants to Be a Millionaire?

This is probably the most basic rule, that generally suggests aspiring retirees should have a million dollars in the bank before they stop working. Yet, these days, this thinking is a bit outdated — as a million dollars certainly doesn’t go as far as it did 20 or 30 years ago. While it may be a good initial goal for some, you’ll want to take a look at your own current and desired lifestyle to roughly estimate your ideal savings amount in order to live most comfortably.

Retirement Tips for Women

Regardless of what plan you choose, the earlier you begin putting money away for retirement, the better. An easy way to get started, even prior to meeting with a financial advisor, is to automate your 401(k), 403(b), or IRA contributions; whatever you can afford to contribute to begin with helps.

In addition, as you approach retirement age, it can also be valuable to look at the ways in which you can optimize social security and maximize your benefits, as social security benefits represent 30% of retirement income for elderly individuals. However, the amount you’re eligible for depends on when you choose to collect your benefits, as well as factors like Medicare deductions and your spouse.

Finally, it’s important to consider your lifestyle goals for retirement. For example, if your plan is to downsize and live pretty frugally, you can aim for a lower savings target. On the other hand, if you want to travel far and wide or treat yourself to luxury vacations, consider ballparking what that might look like for you cost-wise and plan accordingly.

Explore Retirement Resources

Fortunately, there are a number of resources centered around women and retirement savings that are designed for those looking to begin their investing journey, including Ellevest, a wealth management app designed by women, and Female Invest.

If you need to pay down debt or take care of other financial obligations so you can begin saving for retirement, a home equity investment might be able to help you access the cash you need, all without interest or monthly payments.

Take our five-minute quiz to see if a Hometap Investment might make sense for you as you plan for retirement.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

Eugene Wong, Hometap’s new CFO, told the Business Journal that actively seeking an exit or thinking about an exit is not high on the priority list. Needham native Wong officially joined Hometap last month, taking the reins from former chief financial officer Tom Corra.

“An exit is not top of mind for us right now,” Wong, 35, said in a recent interview. “For us, the focus remains growing the business, serving our homeowners and ensuring that we have an A-plus platform that can scale for the future.”

Wong joined Hometap on July 11 from another Boston-based, privately held startup in the fintech space: Forward Financing, which provides funding to small businesses. Instead of small businesses, Hometap offers cash to homeowners in exchange for a share in their home’s future value – an equity share, not debt. The company sees returns when homeowners sell or refinance their properties or buy the company’s equity percentage out.

The majority of our Hometap team finally got together this summer in Boston for two full days of catching up, celebrating the year’s achievements, and soaking up some much-needed facetime. It’s the first time we’ve gone together as a larger group in a year!

Deciding whether to save or pay off debt is a very personal choice — and one that depends on many different factors. However, there are a number of ways to weigh your options in order to pick the best one for you. Below, we’ll cover the pros and cons of each route so you can more confidently answer the question: should I pay off debt or save?

Option 1: Pay Off Debt

Advantages to paying off debt include reducing the amount of interest you’re paying over time, improving your credit score, and lessening the stress and psychological burden that comes along with having the cloud of unpaid financial obligations hanging over your head. It also might make more sense to focus on getting rid of debt if it can help you accomplish some long-held financial goals.

In terms of choosing whether to pay off debt or invest, it may help to know that experts generally advise that if the total interest rate on your debt is greater than 6%, you should pay it down first before focusing on savings or investing.

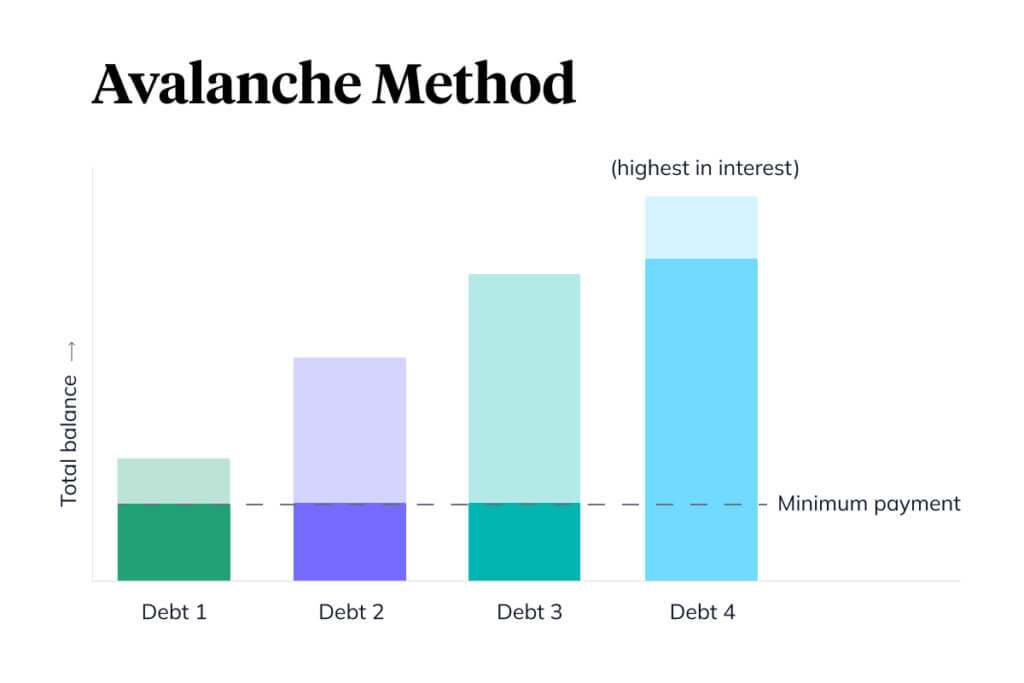

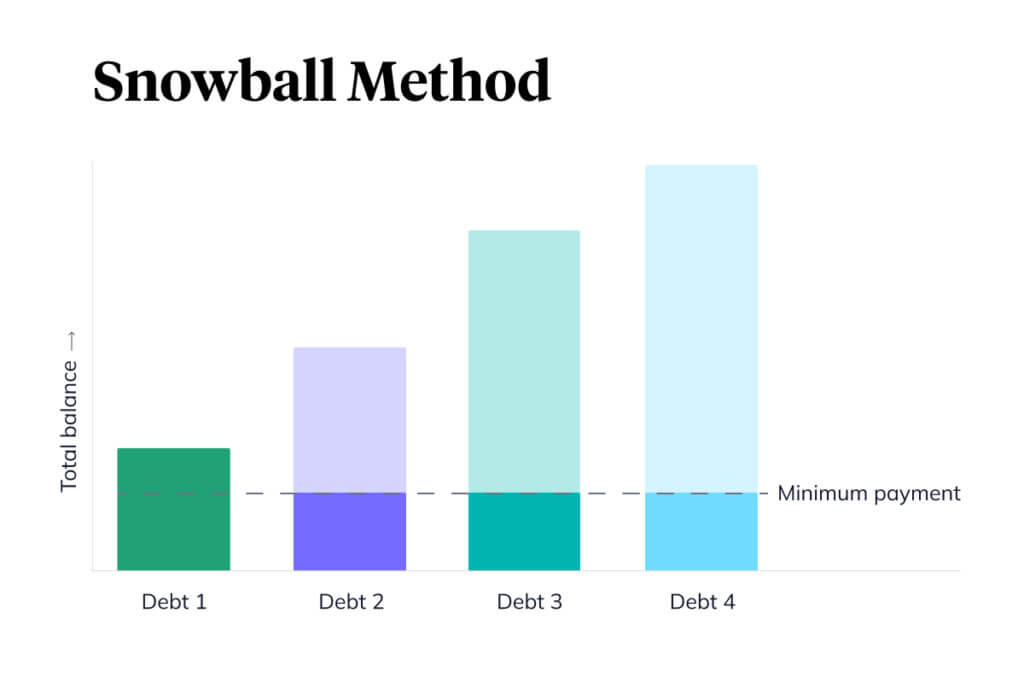

When it comes to how to pay off debt, there are a couple of different approaches you can take. They’re grouped into what’s known as the avalanche and snowball methods.

With the avalanche method, you make minimum payments on all of your debts, and then use any remaining funds to pay off the debt with the highest interest rate. This plan for paying off debt can make the most sense if you’re working toward a long-term goal rather than a short-term financial need.

The snowball method, on the other hand, means that while you make minimum payments on your debts, you then address the smallest debts before taking care of the larger ones. If you’re someone who is inspired to work toward goals by seeing smaller signs of progress along the way, this route might be more appealing to you.

To get a quick idea of which debts may make the most sense to prioritize, a calculator for debt payoff can help. You can plug your current debts, including interest rate and remaining balance, into our Cost of Debt Calculator and get a better idea of how much your obligations are setting you back — as well as how long it will take you to pay them off at your current rate. This tool is also helpful for figuring out which debts to pay off first.

Should I pay off my credit card in full? When should I pay off my credit card?

It’s typically best to keep your credit card paid off for a couple of different reasons. Not only will it help save you money you would be paying in mounting interest payments that add up each month, but unpaid credit card debt can also negatively affect your credit score. If you already have an outstanding balance that you’re able to pay off, it’s a good idea to start here as a first step.

Option 2: Build Your Savings

Choosing to save also has its benefits, however. You may be able to take advantage of compounding interest — the more time your money is in savings, the more your money grows.

You also have better control over your timeline this way, as you don’t have to wait until your debts are repaid to begin getting closer to your bigger goals.

You’ll want to consider what you’re saving up for and whether right now is the best time to pursue it. If it’s your first home, other factors like the current market conditions and the cost of a mortgage versus renting come into play as well, and it may make sense to hold off and handle debts right away.

In any case, setting a target savings goal works toward either a debt payoff or savings strategy, so it often makes sense to begin here no matter what your ultimate objective is — and creating a savings account or emergency fund is a sound decision to avoid debt in the future.

One fairly quick and painless way to begin building your savings is to set up a direct deposit account that automatically puts a percentage of your paycheck into a designated account. If you’re able to afford it, even if it’s a small percentage of your paycheck to start, this can be a smart move.

Another way to save that might seem a bit counterintuitive is to spend money on home improvements that will improve your energy efficiency and cut costs down the road. Even if you don’t make full-scale updates, taking a look at your daily habits with respect to heating and cooling (for example, turning your thermostat down a few degrees or keeping the air conditioner off unless absolutely necessary) can slash ongoing bills and make a difference.

Should I pay off student loans or save?

It can be especially tricky to decide whether to prioritize student loan payments or begin saving, but the most important thing to consider is whether you currently have a comfortably padded emergency fund that will provide a safety net in case of an emergency, or even just a solid cushion in place to handle any major upcoming life events like a move, wedding, or higher education. You should also look at the current interest rates on your loans. If they’re pretty low, you can feel more comfortable starting to save and place your focus back on loans at a later time.

Should I use savings to pay off debt?

Again, it depends. While it can be tempting to dip into your savings to pay off debt, it’s recommended that you maintain a certain amount of emergency funds first before using savings towards debts. Otherwise, you might find yourself unprepared and without enough money to cover an unexpected or emergency situation that arises.

If you decide that paying off debt could help you take steps toward financial freedom, there’s an alternative option to traditional solutions, a home equity investment, that may be a fit. You’ll receive cash in exchange for a share of your home’s future value, and unlike loans for paying off debt, there’s no interest or monthly payments to worry about, so you can start eliminating it more quickly.

Are you a homeowner who could use some extra money to begin chipping away at debt or even add to your savings? Take our five-minute quiz to see if a Hometap Investment might be a good fit for you.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

With a college education becoming more expensive by the year, it can be a challenge to make sense of funding choices and find the right financing fit for your child — or yourself.

Check out this data sheet to learn:

Stats around student loan debt and its effects on other areas of life

The most common college financing options, including federal and private loans

Average costs for in-state tuition and student loan debt by state

American homeowners have never been richer — at least on paper.

After watching their home values soar over the past two years, many owners are looking for ways to tap into their enormous piles of equity.More and more companies are offering to coinvest in owners’ homes, providing immediate cash in exchange for a piece of the property’s value in the future.

Companies like Point, Unison, Hometap, and EquiFi say their products, known as home-equity investments , can help homeowners unlock wealth that’s traditionally been impossible for them to access without selling their homes or taking on more debt. These companies see huge growth potential, since US homeowners are sitting on a record $27.8 trillion worth of home equity, according to the FederalReserve.

As much as we dedicate ourselves to good companies when we work for them, we’re always also in business for ourselves. A human needs to feel growth and opportunities for growth during his or her whole working life, and companies like these that supply those chances at personal advancement liberally are always much sought-for and admired.

What kind of career growth opportunities does your company offer employees?

Opportunities for career growth take many forms at Hometap. We prioritize making learning a habit so that every member of the team is consistently growing, whether it’s strengthening skills for their current role or preparing them for their next one. And our leadership training is as beneficial for our managers as it is for our ambitious teams.