Over the past 20 years, the cost to attend college has skyrocketed. And to make things even trickier, wages aren’t rising at the same pace to offset costs. If you or your child want to pursue a degree but you have no idea how to afford it, you’re not alone.

However, there are a multitude of payment options to help fund education. If you’re a homeowner, you have the added option of tapping into your home’s equity via a HELOC or home equity loan. For many, this is more affordable than high-interest student loans. If you have less-than-perfect credit (anything under 700), you can look to private loan options like a Parent PLUS Loan. You also have a third option that involves no interest or monthly payments: equity sharing.

Before deciding on an option, however, weigh the pros and cons of each as they relate to your financial situation.

Parent PLUS Loan

Best if you have a low credit score

A Parent PLUS Loan is a federal student loan available to biological, adoptive, or stepparents of dependent undergraduate students.

These loans don’t take into account your credit score (though you’ll want to make sure you don’t have an adverse credit history). However, there are several downsides:

You must use the funds for educational purposes.

You don’t have the option for income-based repayment plans.

Interest rates are also significantly higher compared with rates for undergraduate students. Current rates for Parent PLUS Loans are 7.6% compared to 5.05% for federal loans taken on by undergraduate students. That means for a loan of $65,000 you will pay $30,000 in interest over the loan’s 10-year term.

Home Equity Loan or HELOC for College

Best option if you have enough home equity

As a homeowner, you have the option of accessing the equity built up in your home via a HELOC or a home equity loan. You can likely secure lower interest rates with home equity loans and HELOCs than a Parent PLUS Loan. However, rates will depend on your credit score and HELOCs often have variable rates, meaning interest rates may go up.

Unlike a Parent PLUS Loan, you can use the funds however you want—not just on education. For a HELOC of $100,000 with a 10-year draw period followed by a 20-year repayment period, your monthly payments will likely be lower than a Parent PLUS Loan.

Hometap Investment

Best if you don’t want to take on debt

Giving the gift of college to your child doesn’t have to come with the burden of interest-heavy student loans. With no debt, interest, or monthly payments, a Hometap Investment allows you to access your home’s equity in exchange for a share of your home’s future value. It can fund higher education—without having to sacrifice your financial goals (or your child’s).

As a parent, you want to give your child the gift of education and keep them out of debt. However, that doesn’t mean you have to put yourself in more debt. Before making a quick decision that could get you the cash you need, consider your options that will help you fund your goals now and in the future.

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

Small businesses are the heart of the U.S. economy. They make up an incredible 99.9% of all businesses in the country. What they share in common is the blessing—or burden—of a business credit ranking. The health of your score can determine your access to funds. But it’s not the be-all and end-all to your business growth. Read on to understand what business credit is, how to improve your score, and how you can still access cash with a less-than-stellar score.

What Is a Business Credit Score?

Similar to your personal credit score, every business is assessed and ranked. Factors that make up your score include credit utilization ratio (how much credit you have versus how much you’re using), length of credit and payment history, and any outstanding debts, among others. Your score signals to lenders your reliability to repay a loan, otherwise known as your creditworthiness.

Unlike personal credit scores, business rankings use a different scale. While FICO scores range from 300–850, business rankings generally use a zero to 100 range.

Boost Your Business Credit Score

NerdWallet advises the best and perhaps most obvious way to boost your score is to pay your bills on time. Here are some other options to lift your levels.

Pay early. If you’re the type of business that waits until the due date to hit “pay now,” consider breaking this habit. Paying bills early not only positively impacts your credit score but it also signals to your creditors that you’re committed to a good working relationship.

Increase your credit streams. When you’re in not-so-great credit shape, the last thing on your mind is opening a new line of credit. The key, however, is to open that new line of credit—and not use it. Having more credit available increases your attractiveness to credit agencies.

Manage cash flow with your credit card. Business credit cards have come a long way. They offer access to fast financing with low interest rates and flexible grace periods, according to Credit Karma. Business credit cards can also help you manage a positive cash flow. Similar to a personal credit card, charging regular expenses on your business card buys you time before actual cash is due for payment. Some cards will let you carry a balance or delay payment up to 60 days. And, of course, if you’re flush with cash one month, paying your bills early will offset those months when cash is tight.

Fund Your Business—Even With a Low Score

Bad credit doesn’t have to seal your small business fate. Here are three alternative funding sources to fuel your growth.

Borrow from a business credit card. Small businesses are often big spenders, especially when just starting out. That’s one reason why many business credit cards offer borrowing amounts up to $50,000. That may be more than enough to build your business or help you scale. Keep in mind, however, a minimum credit score may be required to qualify.

Explore small business lending platforms. Small business-specific lenders have exploded in recent years. They are a great option for businesses that intend to repay a loan within six to 12 months. Kabbage is one company that dispels with a minimum credit score altogether. Instead, Kabbage requires at least one year in business with a minimum of $50,000 annual revenue and personal guarantees.

Tap into your home equity. Business owners who just happen to be homeowners are in luck. Home equity loans offer an attractive alternative with fast application and flexible terms. Home equity loans are also less dependent on credit score and more dependent on the equity you have in your home.

Another way for near-immediate access to funds is a Hometap Investment, which gives homeowners access to the financial boost their small businesses need without debt, monthly payments, or interest.

Grow at Your Own Pace

Every business experiences financial highs and lows. Your immediate cash need may not match up with a lengthy loan process, however. And, with low credit scores, getting that loan in the first place may be difficult if not impossible. But, with the right strategy in place, you can increase your business credit score, opening the door to more financial options for your small business.

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

It’s a homeowner’s dream: You purchased your home and its overall value is hockey sticking. For Greater Boston residents who’ve owned their home for around 7.5 years, there’s no hyperbole since during that time home values have increased 28%.

But like all homeowners, you must continuously maintain your property. Many are wondering if the upside of a high home value is worth the stressful downside of keeping up the interior and exterior. Read on for guidance on how to approach the decision to stay put or sell.

The Onus of Homeownership

Whether you’re a first-time owner or in your second or third home, the responsibilities of homeownership are perennial. From small, everyday fixes to annual maintenance or surprise repairs, a home is a living thing that needs regular care and attention.

According to a recent Hometap survey, home maintenance and upkeep costs are the biggest source of stress for Greater Boston residents. Nearly three-quarters of those polled identified the tasks surrounding upkeep—landscaping, cleaning, routine home repairs, leaf and snow removal—as nerve-wracking while 63% are worried by the costs associated with maintenance tasks.

How to Get Ahead in Homeownership

The good news for Greater Boston owners is you’re likely sitting on hundreds of thousands of dollars in equity. And the cherry on top is that no slowdown in home values is anticipated in the future. (That might be cold comfort for some faced with major repairs or renovations on the horizon.)

Before you put up the “for sale” sign, consider all your options.

1. Plan Ahead

Do you have a plan of attack for regular maintenance and a smart savings plan? If not, see our expert tips on how to get one started today. It’s easier than you might think.

2. Cut Costs on Your Renovation

The kitchen or bathroom remodel is unavoidable. But cutting costs before and even during your project is doable—without cutting corners. Check out our 10 not-so-secret ways to reduce your renovation expenses.

3. Tap Into Your Home’s Equity

Some homeowners rely on smart solutions like a Hometap Investment to “cash in” on their home’s value. With no monthly payments or interest, Hometap offers homeowners a way to fund the present without risking their future. Learn more about Hometap.

How Much Is Your Home Really Worth?

For many Americans, their home is the biggest purchase they’ll make in their lives. Staying in—or selling—your home is a personal decision with emotional and financial consequences. If you love your neighborhood, your community, and the commute to work, staying put might have more value than you realized. An upswing in your home value is an added perk, too. With a small-step, reduced-stressed approach to upkeep and smart financing, you can stay in your home as long as you choose.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

A reverse mortgage allows homeowners who are at least 62 years old to use home equity to supplement their retirement income. Reverse mortgages, also called home equity conversion mortgages, aren’t like conventional forward mortgages in that you do not make monthly mortgage payments. So, how does a reverse mortgage work?

Instead, as ReverseMortgageAlert.org describes, “the borrower receives payments from the lender and does not need to make payments back to the lender as long as he or she lives in the home and continues to fulfill basic responsibilities, such as payment of taxes and insurance.” As time goes on, the loan balance and interest grows, while home equity decreases.

While this option was perhaps an afterthought for many retirees in the past, the coronavirus crisis has brought it to the forefront once again as a choice for those whose funds were decimated during the economic crash caused by the pandemic. Applications for home equity conversion mortgages (HECMs) increased 15% in March 2020 from the previous month, and up 50% in Q1 from 2019.

“Our customer is the older homeowner that is in their retirement, and their retirement just got pummeled by about 20% or 30%,” he explained. “Our customers are thinking, ‘I should be accessing the equity in my home versus trying to sell off my position or live off my retirement with the notion that over time, it’ll come back.”

Experts believe that the knowledge deficit that existed when reverse mortgages first hit the market has been addressed, leading to fewer cases of cold feet.

“Over the years, what I’ve noticed, especially with borrowers in that 62 to 72 range now, they’re coming in a lot more educated than they had previously been on the product,” Paul Fiore, chief retail sales and operations officer at AAG, told HousingWire. “They’ve done a lot of research, probably online, looked into different things and different aspects of the product. So, they’re coming in more educated, at least in the fundamentals of the loan.”

There are three types of reverse mortgages:

Single-purpose reverse mortgages

This option is typically the least costly, but it has restrictions and might not be the easiest to come by. As the name suggests, the lender dictates the purpose of the loan — for example, to pay property taxes or take care of home repairs. While the qualification criteria makes it fairly easy for most homeowners with low-to-moderate income to get approved, they aren’t very widely available, mainly offered by state and local governments and select nonprofits.

Proprietary reverse mortgages

These are private loans that are funded by the companies that create them. This may be a better choice if you own a high-value home, as you have the potential to receive a higher loan amount than you would with other types of reverse mortgages, especially if your mortgage balance is low.

Home Equity Conversion Mortgages (HECMs)

HECMs are backed by the U.S. Department of Housing and Urban Development (HUD) and are federally insured. There are a few advantages to HECMs: there isn’t a firm income requirement, and unlike single-purpose mortgages, they can be used for any reason. However, they tend to be pricier than old-fashioned home equity loans in terms of both total costs and upfront fees.

Reverse Mortgage Pros

No mortgage payments. A reverse mortgage allows retirees on fixed incomes to stay in their home — with no monthly mortgage payments. The entire loan comes due at the end of the term, generally when the homeowner dies or moves out.

Immediate cash. Many families have little to no retirement savings, according to the U.S. Government Accountability Office. If you’re in a similar boat but have equity in your home, a reverse mortgage can help eliminate or mitigate cash flow issues that can crop up once you’ve stopped working.

Bigger Social Security benefits. A reverse mortgage can allow you to delay drawing on your Social Security, helping you reap bigger benefits down the road. As the Internal Revenue Service lays out, you can get 100% of your benefits at age 66. But you can get 132% of your benefits if you wait to draw funds until age 70.

See how Reverse Mortgages compare to home equity loans, refinances, and other financial products in our Home Equity Investments 101 Guide.

Reverse Mortgage Cons

High fees. According to Reverse.org, reverse mortgage fees are typically higher than those of a traditional mortgage. For example, there’s an initial Federal Housing Administration (FHA) mortgage insurance premium of 2% of the home value, up to $13,593, plus ongoing FHA premiums of 0.5% of the outstanding mortgage balance.

Inability to move. You may not have plans to move. But, as Investopedia cautions, if you have to move into a nursing home or assisted living facility for more than 12 consecutive months, it’s considered a permanent move. Since lenders require you to live in the home you’re borrowing against, you’ll need to pay back the reverse mortgage. If you can’t, then the lender will foreclose on your home.

“When the money runs out, you can’t borrow any more. You can’t dip into that well,” warns Bruce McClary of the National Foundation for Credit Counseling. “And often times what happens is this leaves seniors with their back up against the wall with one less financial option and a home to maintain…it is a back pocket option, and I would say that people should probably save it as something that’s more like a last resort.”

Inheritance is tricky. If you’re hoping to keep your home in your family, your heirs will have to repay the loan balance. Reverse Mortgage Funding says that the loan is traditionally paid off by selling the home or refinancing through a traditional mortgage.

“There are provisions that allow family to take possession of the home in those situations, but they must pay off the loan with their own money or qualify for a mortgage that will cover what is owed,” McClary adds. And while a reverse mortgage refinance is possible, it’s quite uncommon and requires that very specific criteria be met first.

Alternatives to a Reverse Mortgage

Reverse mortgages aren’t your only financing option as a homeowner. Unlike reverse mortgages that require you to be 62 years or older, these financing options do not have age restrictions. Plus, you don’t have to fully own your home (or have a very small mortgage) to qualify as you do with a reverse mortgage.

Home equity instruments. A home equity loan and a home equity line of credit (HELOC) are not the same thing. Although both allow borrowing against the equity in your home, the terms differ. A home equity loan is a lump sum that generally has a fixed rate while HELOC rates are usually adjustable and the amounts are smaller. Both are better suited to filling short-term financial needs.

In addition to considering your long- and short-term financial needs, you’ll want to determine the cost of borrowing, taking into account interest and fees.

Selling your home. If you sell your home — particularly if your mortgage is paid off — and move to a rental property, you can gain a significant bump to your retirement fund. Downsides include monthly rent payments and the loss of property from your estate.

Hometap. For many homeowners, Hometap can offer the best of both worlds. Like a reverse mortgage, a Hometap Investment eliminates monthly payments. But because Hometap is an investment, not a loan, it could be the most affordable option, as you don’t have to worry about paying interest, either.

Unlike some reverse mortgage options, there aren’t any restrictions on how you can use the money, so you can put it toward whatever is most important to you, from renovating your home, to paying down debt, or diversifying your portfolio. Finally, if you’re worried about qualifying for a reverse mortgage, it may help to know that the requirements for a Hometap Investment are unique from a reverse mortgage and traditional loan options.

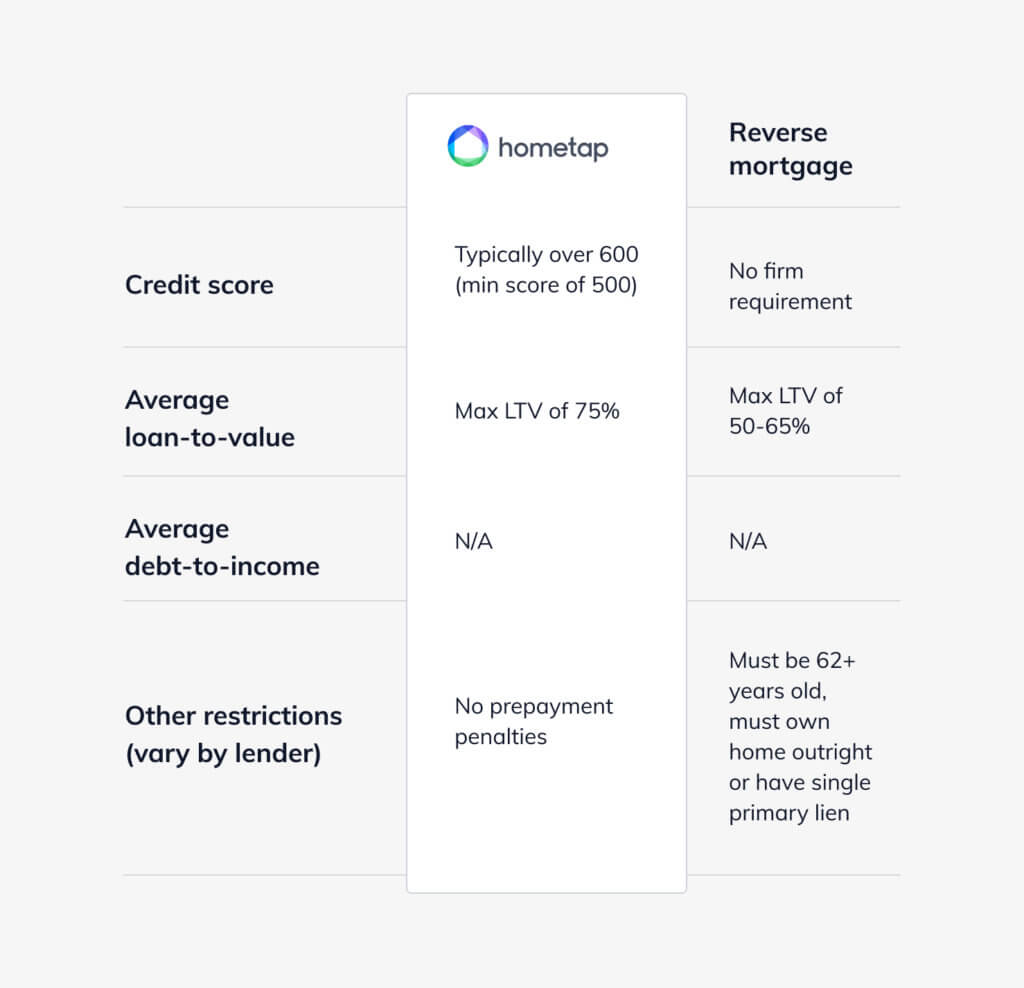

You can quickly compare a Hometap Investment and a reverse mortgage using the chart below.

Everyone hopes they’ve set aside enough money to enjoy retirement, but unexpected expenses or a longer lifespan may leave us needing additional sources of income. Carefully consider the pros and the cons of a reverse mortgage to decide where your home fits into your retirement plan based on your goals and your situation.

Take our 5-minute quiz to see if a home equity investment is a good fit to fund your financial goals.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

With rising taxes, Medicare costs, and interest rates, retirement doesn’t come cheap. More than 1 million reverse mortgages, or Home Equity Conversion Mortgages, have been sold since 1990. But before you decide to fund your retirement via a reverse mortgage, it’s worth weighing the benefits against the risks for your situation, plus exploring alternative ways to fund your retirement dreams.

When to Apply for a Reverse Mortgage

1. You Want to Grow Your Retirement Savings

Since reverse mortgages offer fast cash, you can add that money to your retirement savings. The extra cash allows you to diversify your portfolio and grow your future funds.

2. You Can Cover Closing Fees

As with traditional mortgages, reverse mortgages have their own closing costs. According to American Advisor Group, fees include:

Credit Report: $20–$50

Flood Certification: $20–$30

Escrow Fee: $150–$800

Document Prep: $75–$150

Recording: $50–$500

Courier: $50

Title Insurance: Varies by loan amount and region

Pest Inspection: $100

Survey: $100–$250

You’ll also pay an initial mortgage insurance premium fee equal to 2% of your home’s value, plus a loan origination fee charged by your lender starting at 2% of the loan with a maximum of $6,000. It’s possible to roll many of these costs into the reverse mortgage itself, but a home appraisal—$400–$600—must be paid upfront.

When to Steer Clear of a Reverse Mortgage

1. You May Need to Leave Your Home

Reverse mortgages are not forgiving if unexpected health issues arise. That means if you need to move into a nursing home or assisted living facility, the loan will need to be paid upfront. (A leave of absence longer than 12 consecutive months is considered a permanent move by law.)

It’s difficult to plan for future illness. Take the time now to ask yourself the tough questions about if or when you’d need to leave your home.

Reverse mortgages have no monthly payments, but they do require homeowners keep up with other related costs. These range from home maintenance, property tax, and insurance. Unfortunately, more and more seniors are facing foreclosure from reverse mortgages because they fell behind or failed to meet other requirements.

Alternative Retirement Funding Options

1. Personal Loans

Personal loans are beneficial for paying down debt in a number of ways. Not only will your credit score rise from lowering your debt but you can apply for a lower-rate reverse mortgage later if it’s a fit to fund your retirement.

2. Equity Investments

Home Equity Investing is exactly what it sounds like. Homeowners tap into their home’s equity in exchange for a share of the property’s future appreciation or depreciation.

A Hometap Investment is an equity investment that allows you to fund your retirement and stay in your home—without any monthly payments or interest. And unlike other options, you don’t need to sell your home when your term ends; you can refinance or buy out the Investment with savings instead.

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

The average home renovation project lasts six to eight months and involves around 15,000 decisions. Sometimes hiring a professional to guide you, keep you on track, and make some of those decisions is worth the investment.

A home renovation consultant, also referred to as a home renovation coach or a home improvement consultant, is essentially an expert project manager for your home remodel or renovation. But what exactly does a home renovation consultant do and do you need one? Read on as we explore a typical consultant’s role and the types of projects that benefit from one.

What Is a Home Renovation Consultant?

A home renovation consultant advocates for you and your project by hiring and managing the right people for your renovation job. This professional isn’t a contractor or architect but rather helps with the budget, design, vendor meetings, and/or material selection. They may guide you from start to finish or put you in the right direction.

While costs vary depending on the consultant and the project, Realtor.com spoke with several professionals and found base packages starting around $250 for initial design consultations. Larger projects, like a complete kitchen remodel lasting two to three months, can cost anywhere from $3,000 to $5,000.

When to Hire a Renovation Consultant

When is it worth it to spend $250 to $5,000 or more? Larger projects that require multiple vendors are a prime example of when a home renovation consultant can save you time and possibly money in the long run.

Rather than carving out the time to manage multiple vendors on your own, the home improvement consultant can provide you with unbiased advice and connect you with professionals suited to your project. By giving you a realistic picture of what it’ll take to complete the project and connecting you with the right people upfront, the renovation consultant can save you from costly do-overs and mistakes.

If you have trouble staying on budget, you may want to consider a renovation consultant. The consultant can develop a realistic budget at the beginning of the project so you know what to expect rather than later facing a half-completed project and vendors telling you it’s going to cost more than anticipated. This person can also keep the project on task, ensuring vendors—and you—are always working toward your ultimate end goal versus getting sidetracked.

One of the most valuable things a home renovation consultant can bring to your project is their network of trusted vendors, from architects and general contractors to designers and materials specialists. If you don’t know what professional(s) to hire for what portion of your project, you can hire a consultant to point you in the right direction.

When You Can DIY

If your budget is tight and you can reasonably find time to manage the project, then you may consider forgoing the services of a renovation consultant. However, you may find it’s worth making room in your budget for a renovation consultant if only to ensure you’re plotting a course that will get the project done right the first time—and keep you within budget.

Small, weekend jobs also don’t warrant a renovation consultant. Of course, if the job ends up going off the rails in a weekend, it’s not too late to hire a renovation consultant to assess the situation, mitigate any disputes, and provide you with the most cost-effective path for getting your project back on track.

Before you assume that you can cut corners and forgo the initial cost of a renovation consultant, take a step back from your project. Do you know what kinds of professionals you need for your project? Do you have a professional you trust? Could you have blind spots that would benefit from an unbiased outside opinion? Sometimes the small, simple projects are the ones that can easily get off-track. The added upfront cost of hiring a renovation consultant may save you from unexpected costs later in the project.

Did you know the equity in your home could fund your renovation? Learn how home equity investments compare to renovation loans, lines of credit, and other solutions for funding your home remodel.

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

How much could you save on your mortgage with an improved credit score? A lot, it turns out.

According to BankRate, your credit score is one of the top factors that lenders consider when setting your interest rate. A solid score indicates to lenders that you present less of a financial risk and they reward that track record with generous loan terms. Credit.com reveals that loan officers also compare credit score and the loan-to-value ratio to determine interest rate adjustments.

It’s no secret that the closer your score is to 800, the odds of home loan approval go up and interest rates go down. But just how much of a score increase do you really need to see a significant difference?

Small Changes, Big Difference

On the vast scale of 800, a handful of points here or there may not seem like much. As such, most of us are focused on those big, hundred-point jumps that get us out of the garden-level apartment (500) and into the higher-rent districts (600, 700) or even the penthouse (800).

But it’s crucial to remember that the lending industry measures in 20-point increments and adjusts rates accordingly. This means a drop from 780 to 760 will likely result in higher costs that grow even higher for every level you go down. This system, as NerdWallet explains, is known as loan-level pricing. As 20, 40, 60 points start to rack up, you’ll find yourself talking about real money very quickly.

If your score drops by 100 points or more, the landscape can change completely. This is particularly true over the long view of 30 years when you may end up owing tens of thousands more in loan payments.

In short, your credit score is money. The better it is, the more you’ll have. It, therefore, pays off in the long run to be vigilant—handle debt responsibly, don’t spend beyond your means, and do your best to pay all bills on time and in full.

Whether you need a loan to consolidate debt or pay down bills, Hometap can be a smart option for homeowners looking to cash in on their equity without monthly payments or interest.

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

An inspected furnace is an efficient furnace, leading to a toasty home and reduced heating bills. Additionally, an inspected furnace preserves your household health, since clean filters minimize air particle buildup and well-sealed vents reduce the risk of carbon monoxide poisoning. Spending around $100 (the national average, plus the cost of new filters) to get your furnace inspected and tuned up can provide incalculable savings to both your home and well-being.

What to Do

Ensure your furnace is in good working order prior to heavy use this winter.

What You’ll Need

The Basics

Dust mask

Gloves

The Works

New air filter

Foil tape

Vacuum

How to Do It

In most cases, you should hire a professional to do a full furnace inspection and make any needed repairs. Beforehand, however, there are a few steps homeowners can take for a preliminary check.

All Furnaces

Go down to your furnace and look at the burner flame. Ideally, the flame should be steady and blue. If the furnace is running, listen for any unusual noises or vibrations.

Turn off both the fuel supply (gas line or oil burner) and power source to your furnace.

Locate the air filter and determine if it should be replaced. Purchase the appropriate size replacement filter from your local hardware store. Carefully remove the old filter and replace it with the new one. Discard the dirty filter.

Check the furnace’s flue pipe for any cracks or breaches. Minor breaches can be closed with foil tape whereas large cracks will require a full pipe replacement.

Gas Furnaces

Smell the area around the furnace for any gas odors. Check the batteries in your home’s carbon monoxide detectors and replace as needed. If anything seems off, call a furnace technician immediately.

Oil Furnaces

Check to see when you last had your oil filter changed on your furnace. If it’s been awhile or you can’t remember, schedule a filter replacement as part of an inspection.

Restore the fuel and power to your furnace.

If your heat is circulated through floor vents, remove their screens and vacuum out any collected dirt and debris. Wipe down screens and replace securely. Discard all collected dirt and dust.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

The holidays are coming! If you’re hosting friends and family this year, you know the preparations go way beyond the menu. There are guest rooms to clean and tidy up, decorations to unpack and arrange just so, extra groceries to buy and cook, and gifts to get (and wrap). While there’s a lot to do, it can all come together smoothly with minimal stress—we promise!

Grab a cup of coffee and peruse how these home and entertaining experts get their abodes ready for holiday guests.

Get Your Guest Rooms Ready for the Holidays

Add a little Southern hospitality to your guest room with tips from Southern Living, including putting out travel-sized toiletries (arranged in a pretty basket, of course), extra blankets, and a notebook with the house’s Wi-Fi password.

To help guests settle in, keep toiletries in plain sight, give your guests a set of spare keys, and offer a few types of pillows, says Alexis Hobbs at Woman’s Day.

Make your guests feel at home by giving them the best bed money can buy, says the team at The Spruce. This means top-of-the-line mattresses and pillows with premium linens to ensure visitors get a good night’s sleep.

Tackle Your House Projects before Guests Arrive

If you’ve been neglecting a few small repairs around the house, now’s the time to take care of them, says the team at Housetopia. Filling in dents and cracks, adding a fresh coat of paint, and creating inviting gathering spaces will make your home look pristine and your guests feel welcome.

Standout tips in Houselogic’s “6 Simple Steps to Prep Your Home for Holiday Guests” include banishing all clutter, adding night lights (especially in hallways and bathrooms), and creating a coffee station for your guests.

Don’t have a guest room? Real Simple to the rescue! Their “20 Ways to Make Guests Comfortable When You Don’t Have a Guest Room” story is a must-read for thoughtful hosts who just happen to have small spaces.

Watch the Pros at Work

If you need to have an existing room double as a guest room, check out how Meg Allan Cole with HGTV Handmade transformed her apartment’s always-office into a sometime-guest room.

Seal those drafts and get cozy sheets! Maxwell Ryan of Apartment Therapy partners with Better Homes & Gardens on a video with quick and practical tips for “How to Prep Your Guest Room for the Holidays.”

Opting for a day bed, getting cabinets with both shelves and drawers, and putting storage cubes to good use are just a few good tips from Lowe’s “5 Ideas for Decorating a Guest Room” video.

We’ve already started reconfiguring our guest rooms and picked up a few new throw pillows and linens. Which holiday hosting tips will you put to use in your own home this year?

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

A few years ago, an unnamed, first-time homeowner member of the Hometap team didn’t realize this important task needed to be done and, come winter, had a burst pipe in the basement when the pipe’s residual water froze and expanded. Hours of cleaning and a hefty plumbing repair bill later, they’ve never made that mistake again! With burst pipe repair costs ranging from $500 to $3,800, taking an hour or so to drain your exterior pipes this weekend will grant you peace of mind and save you money once freezing conditions settle in.

What You’ll Need

The Basics

Gloves

Bucket

What to Do

Turn off the water supply and drain all residual water in pipes connected to outdoor faucets.

How to Do It

Identify each faucet around the exterior of your property and remove attached garden hoses (as applicable). Drain remaining water from hoses, then roll them and store away for the winter. Choose a faucet to address first (if you have more than one) and make sure it’s in the off position.

Locate the water supply valves to each exterior faucet and shut them off. (They’re typically found on or near the basement ceiling or next to the main water supply valve.) Once the water supply has been shut off, go back outside to the exterior faucets. Place a bucket under each and turn the faucets on to drain any residual water. Once excess water has been drained and collected, dump the bucket. Leave the faucet in the on position.

Go back inside with your bucket to the interior pipe’s water supply valve and locate the bleeder cap. Holding the bucket underneath the valve, unscrew the bleeder cap to drain the remaining water out of the pipe. Once all water has been drained, replace the bleeder cap and fasten tightly. Go back outside to drain the bucket and turn the faucet off.

Repeat this process with each exterior faucet around your property.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.