While rising home prices and interest rates have presented major challenges for prospective homebuyers, homeowners in many parts of the country are sitting on record-high amounts of equity. In Q1 of 2022 alone, equity jumped 32.2% and national homeowner equity grew $3.8 trillion — with the average homeowner gaining $64,000. While there are a few different factors at play, including those skyrocketing home prices, low inventory, and a surge of renovations and remodels spurred by the pandemic, the end result is a whole lot of equity for a whole lot of people.

Here are the 10 states where homeowners have gained the most equity this year.

The average California homeowner has gained $141,000 year over year from the first quarter of 2021. California also has some of the highest home values in the entire country, with a median home price of $799,311 — an 18.5% jump between June 2021 and June 2022.

Homeowners in Hawaii gained $139,000 in equity on average between 2021 and 2022. Hawaii is also known for its high home values, with the typical price coming in at $901,942. Home prices shot up 22.1% year over year between June 2021 and June 2022.

In Washington, the average homeowner’s equity grew $114,000 in 2022. The typical home value here is $627,555, a 21.2% increase year over year from June 2021 to June 2022.

Arizona homeowners earned an average of $96,000 in equity from Q1 2021 to Q1 2022. And while the typical home value in Arizona — $450,629 — is significantly lower than states like California and Hawaii, prices have surged 26.3% in one year. Arizona homeowner David was able to use his equity to fund an investment property with a Hometap Investment. Read how he did it.

Colorado

Homeowners in Colorado experienced a $92,000 average equity increase this year. Here, the typical home value is $591,189, and prices have surged 21% from June 2021 to June 2022.

More than ever, homeowners have the opportunity today to tap into their equity to reach their financial goals — from paying down debt to making much-needed renovations or funding an education.

Are you a homeowner who wants to make the most of your equity? Take our five-minute quiz to see if a Hometap Investment might be a fit for you.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

Today’s real estate market has a lot of homeowners debating whether they should cash in on their home’s appreciation by selling their home or accessing their home equity. There are several factors to consider that can help you make the decision that’s right for you. Below, explore the advantages and disadvantages of each option, as well as the most common ways to access your equity so you can answer the question Should I sell my home? with confidence.

Selling: Pros and Cons

While the idea of downsizing to a smaller home or conversely, finding a house with more space to spread out may seem appealing in theory, the current market can make it a whole lot tougher in reality.

At the moment, the real estate market is red-hot, with a median sale price of $370,528 — an increase of more than 22% year-over-year from April 2020. More than 600,000 homes sold in the U.S. in April, a jump of 38.2% from the previous year. Mortgage rates have also dropped 0.2 points, making it more tempting than ever for prospective (and stir-crazy) buyers to lock in an offer on a new house.

Often, short-term financing solutions like bridge loans can allow buyers to forego the contingencies and move more quickly, which can be a huge plus in a hot market. But it comes with risks, too. Some contingencies include forgoing home inspections, which may end in buyers’ remorse for those urgent to move into a new home.

There’s also the costs of moving to consider. If you plan on hiring movers, the average price tag is more than $1,000, depending on how much you’re taking with you. And of course, that’s not taking into account the hassle and emotional toil of the whole process.

In short, those looking to downsize or move to a location with a less competitive market have a great opportunity to cash in on a hot market, but it’s important to have a strong handle on your numbers and your moving plan.

Tapping into Your Equity: Pros and Cons

Moving isn’t the only way to make the most of your home’s growing value. You might be able to transform your current home into your dream home by tapping into your hard-earned equity to make the renovations you’ve been putting off — or build a long-desired addition.

If you decide that you want a seasonal getaway, you can also use your equity to put a down payment on a vacation home. There are a handful of different ways to get equity out of your home. Let’s explore the most common ones.

Home equity loan

One of the most common ways homeowners tap into their equity is through a home equity loan, as its fixed rate and lump sum payment often makes sense for funding home improvement projects. However, the qualification and approval process can present hurdles, as most lenders require a firm minimum credit score and stringent criteria.

HELOC

You can also open a home equity line of credit (HELOC) to access your home equity. This option offers flexibility in terms of the amount of money and how often you can borrow, but also comes with a level of unpredictability due to rate variability. It can also be risky because your lender can freeze your HELOC if your credit score or home value decreases.

Cash-out refinance

A cash-out refinance is another popular option for tapping into your equity. If you go this route, you have the chance not only to cover the cost of your renovation, but also to secure a lower interest rate on your mortgage. However, since you’re essentially paying off your mortgage with your current one, your timeline will be extended and you’ll have to pay application, closing, origination, and possibly even appraisal fees.

With a home equity investment, you can get a portion of your equity in cash in exchange for a percentage of your home’s future value — usually within a few weeks. You don’t have to deal with any monthly payments or interest, and can use the funds for whatever you’d like. This solution allows you to stay in your home and bypass the challenges and extra costs associated with moving.

Ultimately, Should I sell my home or tap into my equity? is a question only you can answer based on your own financial and personal situation.

Take our five-minute quiz to see if a Hometap Investment might be a good fit for accessing your equity without having to sell your home.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

You’ve heard the term, but what is home equity, exactly, and how is it calculated? Home equity is the value of a homeowner’s interest in their home, and it’s important to keep track of because home equity provides opportunity for homeowners. This number changes over time due to both market shifts like local and national trends, as well as your own mortgage payments; the more you’ve put toward your home, the more equity you’ll have. Here we’ll cover how to calculate home equity, and how to use it.

Why Is Home Equity Important?

Building equity in your home is important for a few reasons. First, it counts toward your net worth because unlike nearly every other asset you buy with a loan, your home can still grow in value after you pay it off. You can also borrow your equity to handle life expenses like home renovations, a down payment on a second home, or to fund education — more on this later. Finally, when it comes time to sell your home, the more equity you’ve built up, the more profit you could make on the home.

How Long Does It Take to Gain Equity in a Home?

While there are factors that can expedite how quickly your home accrues equity (like the market shifts we mentioned previously), home equity does generally take time to build, so it should be part of a long-term wealth strategy rather than a short-term plan to get cash.

Homeowners that don’t know how much equity they have are also less likely to know how much debt they have. See more insights like this in our free Homeowner Report.

What is the Formula for Home Equity?

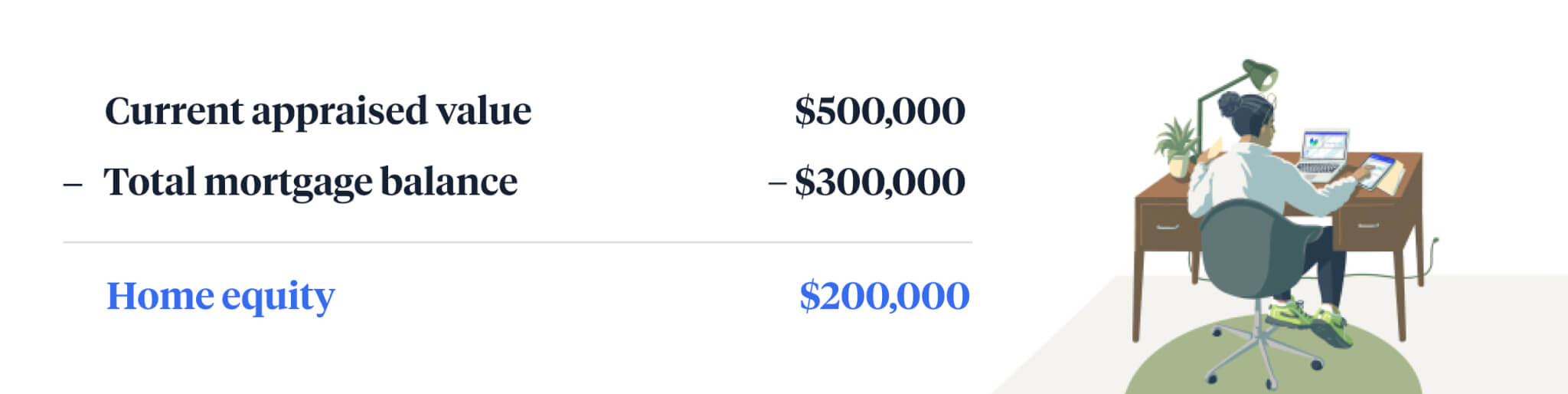

Fortunately, you don’t need a fancy home equity calculator to figure out how much equity is in your home. To find your home equity, simply subtract your total mortgage balance from the current appraised value of your home.

How to calculate home equity:

If you’ve been in your home for a while and aren’t quite sure of the current appraised value, there are a few different ways to go about determining it, short of scheduling a formal appraisal. You can start by looking at nearby “comps,” or comparable homes in your area that have similar square footage, number of bedrooms and bathrooms, and floor plans.

You can also look at the cost-per-square foot of your home and find an average. This is also pretty easy to do: simply divide the selling price of your home by the total square footage.

Once you have a general idea of your home’s current appraised value, you can subtract your mortgage balance to find your home equity.

If you’re curious about the rate at which your home might change in value over time, a home appreciation calculator can help.

How Can I Access My Home Equity?

Now that you know how to determine your home equity, it’s just as important to know to access it. There are several paths to tapping into your home equity, and each comes with pros and cons. Here are some of the most common ones:

Home equity loan

A loan thatoffers a predictable monthly payment, fixed rate, and a lump sum payment.

Home equity line of credit (HELOC)

A revolving line of credit that gives you access to cash through a portion of the equity you’ve built in your home.

Cash-out refinance

A mortgage that replaces your existing one and exceeds your loan balance, providing the difference in cash.

Reverse mortgage

A loan for homeowners 62+ in which the lender pays the borrower in exchange for the home’s equity.

How Can I get Equity Out of My Home without Refinancing?

There is one more financial product that doesn’t involve loans or refinancing your home, which means you can keep your interest rate locked in without adding another mortgage or another debt to your bottom line.

Home equity investments

This loan alternative gives you near-immediate funds in exchange for a share of your home’s future value without having to sell your home or take on more debt. There are no monthly payments and no interest.

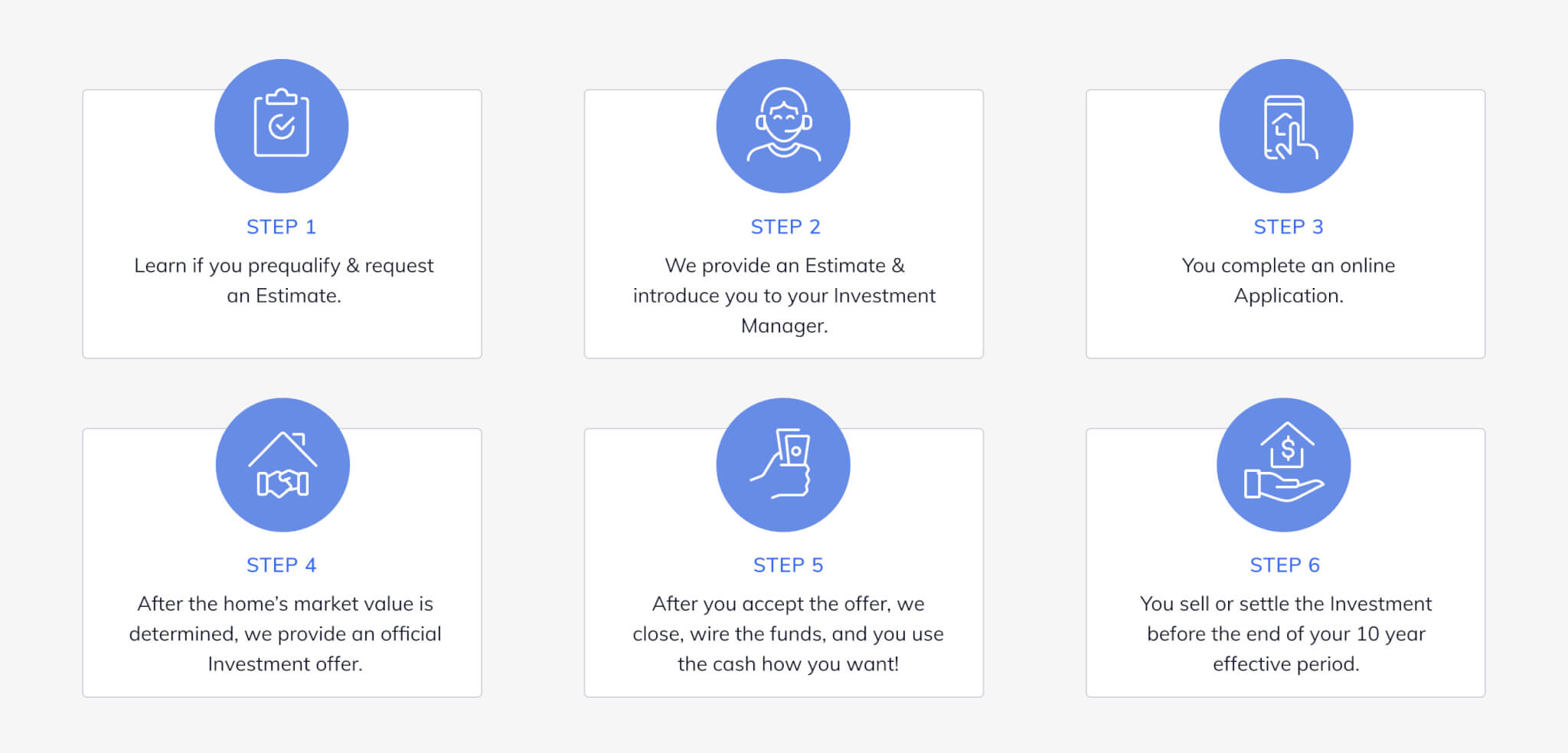

See how a Hometap Home Equity Investment works below:

How Much Equity Can I Borrow From My Home?

This answer will vary slightly depending on which financial product you choose to access it, but generally you’ll need to maintain at least 15-25% of your home equity. For example, if you have 50% equity in your home now, you’ll likely find that you’re able to receive 25-35% of it.

How Can My Equity Work for Me?

While there are many ways to use your home equity — and a home equity investment lets you use it for anything you’d like — it can pay off in the long run to be thoughtful and strategic about where you decide to put the funds you receive. For example, using the money to make home improvements that will potentially add more value to your home is probably a wiser decision than spending all of it on a lavish vacation or a shopping spree. Here are some possibilities to consider:

Pay Off Debt

Paying down debt, including credit cards and student loans, is one of the biggest reasons why homeowners access their equity. And with a home equity investment, this can be even easier to do, since there aren’t any monthly payments to deal with.

Renovate Your Home

Another common use for equity is home improvement and renovation projects. The benefits of this are a few fold: first, you’ll have the satisfaction and enjoyment of that dream kitchen or pretty patio. As we mentioned above, it’s also possible that the renovation will allow you to receive more money for your home if you decide to sell down the road.

Buy a Second Home

Have you always dreamed about a vacation home? How about an investment property that brings in additional income? You can put your equity toward a down payment on a second property. Besides having a go-to getaway spot, you’ll be diversifying your portfolio with real estate as well.

Fund Your Business

Many homeowners use their home equity to start or grow their small business without the hassles of a loan (and the hurdles that come along with getting approved for one).

Live Comfortably in Retirement

If you’re looking for a way to fund current — or future — expenses that your retirement savings can’t cover, like health care, your home equity can save the day and give you peace of mind, along with some extra cash. This is especially attractive if you plan to sell the home within the next 10 years. Though it isn’t required to sell, it may be beneficial to use the proceeds from the sale of the home to settle the Investment.

Fund an Education

With college tuition increasing every year, it can be a smart move to tap into your equity to help pay for your child’s education or start to chip away at that student loan debt.

Diversify Your Portfolio

Many homeowners use home equity investments to balance out their portfolio. A well-rounded portfolio includes a variety of investments that span across at least a few different sectors, including stocks, bonds, mutual funds, and real estate. By distributing your assets, you decrease the risk of a major loss in any one particular area.

Life is full of unexpected events. Whether you need cash, fast, to pay for medical bills, or deal with other surprise costs that pop up, your home equity can get you money in a pinch.

These are just some ideas for how you can use your equity to live a less stressful life — and a home equity investment can help you do it without taking on debt, worrying about monthly payments or interest, or having to sell your home. Now that you know how to calculate your home equity, what it is, and why it’s important, it’s time to decide how you’ll use it!

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

When it comes to financing your home, one size doesn’t fit all. And while traditional options like loans, home equity lines of credit (HELOCS), refinancing, and reverse mortgages can work well for some homeowners, the recent rise of loan alternatives like home equity investors and other emerging platforms have made it clear that there’s a growing demand for other choices. Learn more about alternative ways to get equity out of your home, so you can make a more informed decision.

Traditional Options: Pros and Cons

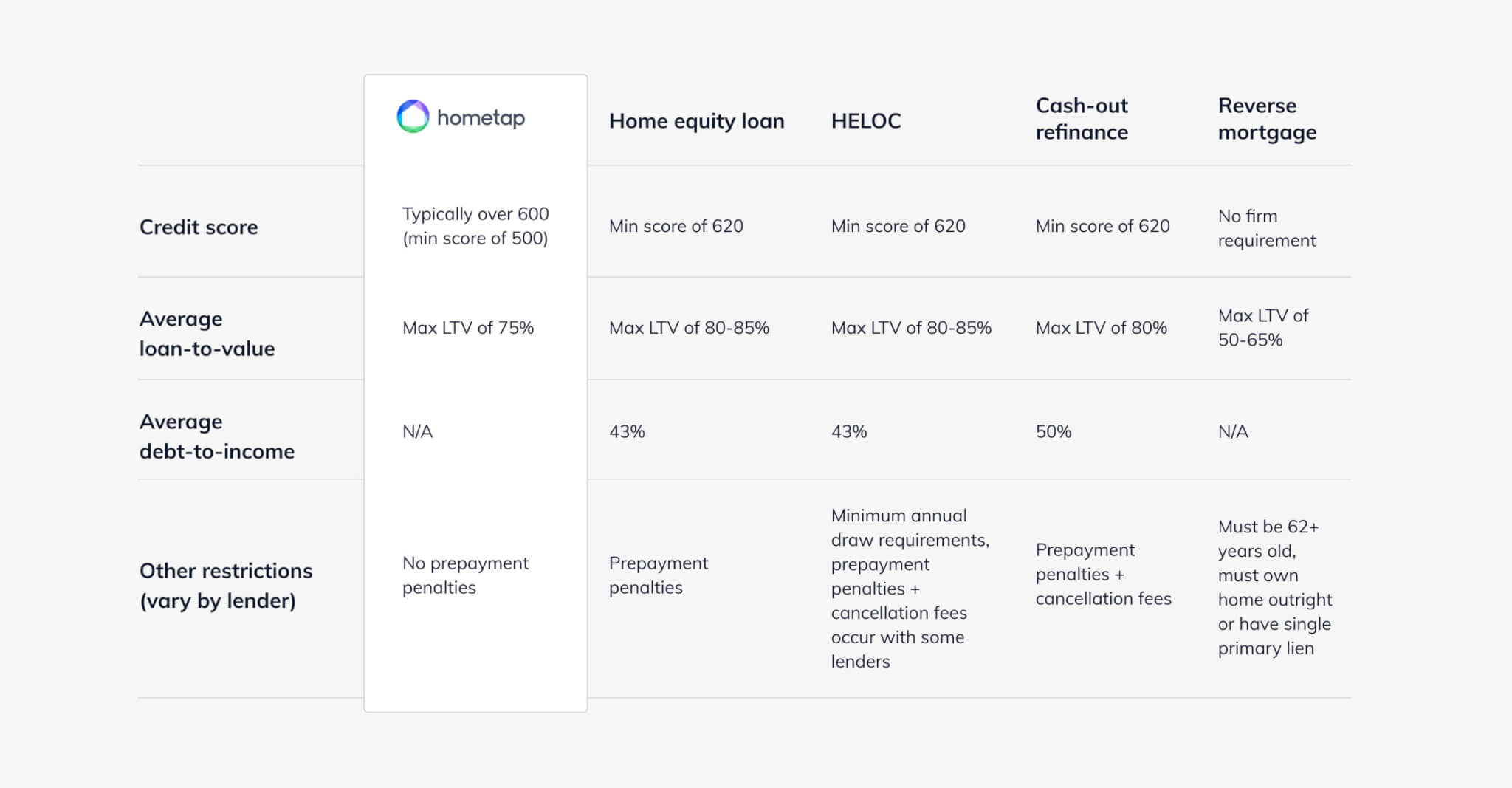

Loans, HELOCs, refinancing, and reverse mortgages can all be attractive ways to tap into the equity you’ve built up in your home. However, there are often as many disadvantages as there are benefits — so it’s important to understand the pros and cons of each to understand why some homeowners are seeking financing alternatives. See the chart below to quickly compare loan options, then read on for more details on each.

Home Equity Loans

A home equity loan is one of the most popular ways that homeowners access their equity. There are certainly advantages, including a predictable monthly payment due to the loan’s fixed interest rate, and the fact that you’ll receive the equity in one lump sum payment. For this reason, a home equity loan typically makes sense if you’re looking to cover the cost of a renovation project or large one-off expense. Plus, your interest payments may be tax-deductible if you’re using the money for home improvements.

Why search for a home equity loan alternative? A few reasons: First, you’ll need to pay off the loan in addition to your regular mortgage payments. And if your credit is less-than-excellent (under 680), you may not even be approved for a home equity loan. Finally, the application process can be invasive, cumbersome, and taxing.

Home Equity Lines of Credit (HELOC)

HELOCs, a common alternative to a home equity loan, offer quick and easy access to funds any time you need them. And while you typically need a minimum credit score of 680 to qualify for a HELOC, it can actually help you improve your score over time. What’s more, you might be able to enjoy tax benefits — deductions up to $100,000. Since it’s a credit line, there’s no interest due unless you take out money, and you can take out as much as you want until you hit your limit.

But with this flexibility comes the potential for additional debt. For example, if you plan to use it to pay off credit cards that have high interest rates, you can wind up racking up more charges. This actually occurs so frequently that it’s known to lenders as “reloading.”

Another major downside that may encourage homeowners to seek a HELOC alternative is the instability and unpredictability that comes along with this option, as the variability in rates can lead to fluctuating bills. Your lender can also freeze your HELOC at any time — or reduce your credit limit — in the event of a drop in your credit score or home value.

Discover how common it is for homeowners like you to apply for home loans and HELOCs, in our 2021 Homeowner Report.

Cash-out Refinance

One alternative to a home equity loan is a cash-out refinance. One of the biggest perks of a cash-out refinance is that you can secure a lower interest rate on your mortgage, which means lower monthly payments and more cash to pay for other expenses. Or, if you’re able to make higher payments, a refinance might be a good way to shorten your mortgage.

Of course, refinancing has its own set of challenges. Since you’re essentially paying off your current mortgage with a new one, you’re extending your mortgage timeline and you’re saddled with the same charges you dealt with the first time around: application, closing, and origination fees, title insurance, and possibly an appraisal.

Overall, you can expect to shell out between two and six percent of the total amount you borrow, depending on the specific lender. Even so-called “no-cost” refinances can be deceptive, as you’ll likely have a higher rate to compensate. If the amount you’re borrowing is greater than 80% of your home’s value, you’ll likely need to pay for private mortgage insurance (PMI).

Clearing the hurdles of application and qualification can lead to dead ends for many homeowners who have blemishes on their credit score or whose scores simply aren’t high enough; most lenders require a credit score of at least 620. These are just some of the reasons homeowners may find themselves seeking an alternative to a cash-out refinance.

Reverse Mortgage

With no monthly payments, a reverse mortgage can be ideal for older homeowners looking for extra cash during retirement; a recent estimate from the National Reverse Mortgage Lenders Association found that senior citizens had $7.54 trillion tied up in real estate equity. However, you’re still responsible for the payment of insurance and taxes, and need to stay in the home for the life of the loan. Reverse mortgages also have an age requirement of 62+, which rules it out as a viable option for many.

There’s a lot to consider when looking at traditional and alternative ways to access your home equity. The following guide can help you navigate each option even further.

Looking for an Alternative? Enter the Home Equity Investment

A newer alternative to home equity loans is home equity investments. The benefits of a home equity investment, like Hometap offers, or a shared appreciation agreement, are numerous. These investors give you near-immediate access to the equity you’ve built in your home in exchange for a share of its future value. At the end of the investment’s effective period (which depends on the company), you settle the investment by buying it out with savings, refinancing, or selling your home.

With Hometap, in addition to an easy and seamless application process and unique qualification criteria that is often more inclusive than that of lenders, you’ll have one point of contact throughout the investment experience. Perhaps the most important difference is that unlike these more traditional avenues, there are no monthly payments or interest to worry about on top of your mortgage payments, so you can reach your financial goals faster. If you’re seeking alternative ways to get equity out of your home, working with a home equity investor might be worth exploring.

Is a Hometap Investment the right home equity loan alternative for you and your property? Take our five-minute quiz to find out.

YOU SHOULD KNOW

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

You know some of the more obvious factors that tend to cause a home’s value to increase or decrease: adding onto the home to turn a two bedroom into three will likely increase its value. Ignoring signs of flood damage and putting off needed maintenance will likely hurt its value. But there are less obvious factors every homeowner should know, too. By understanding what causes your home value to appreciate, you can take full advantage of one of your most valuable assets.

What Impacts Your Home’s Value?

There are several factors you have little to no control over that can impact the value of your home, including time, neighborhood, state, and national trends.

Time

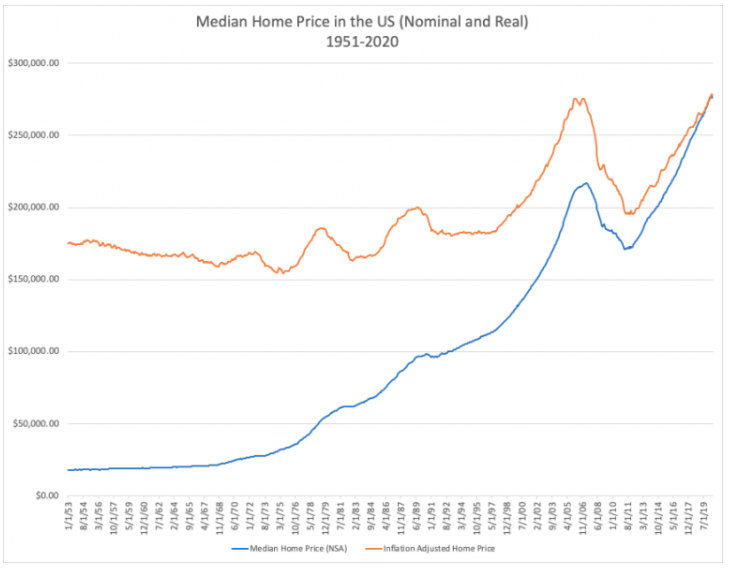

The good news is with regular maintenance, your home value will likely increase over the long run. Data from theUnited States Census Bureau shows that the average price of houses sold at the beginning of 2010 was $275,300, whereas by the third quarter of 2019 prices averaged $380,300. The average home sold for more than $100,000 more than its purchase price within the decade.

Even when taking the 2008 housing market crash into account, most homeowners saw those home values rebound beyond pre-recession levels (with the exception of a few states). The following graph from DQYDJ.com illustrates how median home prices have grown since 1953.

source: dqydj.com

You can find out how much your home has appreciated over time by looking at how much it has sold for over the years, how much you paid for it, and how much it is valued at now. Without hiring a professional appraiser, it’s hard to know your home’s value. But you can start to get a sense by looking at nearby comps, or comparable homes that have recently sold in your area.

Beyond time, neighborhood, state, and even national trends can impact home values. Your neighborhood has the most direct impact on your home’s value. When appraisers look at your home’s location, they’re looking not only at where it physically sits—next to a highway onramp, near public transit, on a quiet dead end street—but also what’s around it. This includes school quality, job opportunities, crime statistics, and what amenities—shopping, entertainment, recreation—are nearby.

State Trends

As certain cities and states become more expensive, people begin to look to other areas. As theNational Association of Realtors shows, certain states have higher job growth than others. Nevada, Utah, Arizona, Idaho, and Texas are some of the states with the strongest job growth from August 2018 to August 2019. They also happen to be the top five states in population growth by percentage between July 2018 and July 2019 according to theUnited States Census Bureau. The growth in population drives the demand for places to live, which of course drives up demand for homes, and home prices.

National Trends

National trends play a part in home values at a macro level. In a sluggish economy, fewer people are looking for homes, slowing the sale of homes and, with that, slowing the rise of home prices.

Similarly, interest rates impact who can afford to buy a home. As interest rates rise, fewer people can afford to buy a home. Fewer buyers means more supply than demand, leading to lower home values.

Can You Increase Your Home’s Value?

Fortunately, there are many elements of your home’s value you can control. Your home’s value is significantly impacted by how well you take care of it. Consistently performing basic upkeep tasks each month can help you maintain the value of your home (not to mention save you money from costly repairs).

Testing your sump pump, sealing your windows, inspecting your furnace, and patching your driveway, among other tasks, can help you keep your home in tip-top shape.

Sometimes, your home will need more substantial improvements. Home buyers, even those open to a fixer-upper, will expect solid structural elements like a sturdy foundation and roof. Some home improvement projects are proven to increase home value more than others: anew garage door has a 97% return on investment! If you have multiple projects on your to-do list, start with the projects that give you the most value for the cost.

However, it’s just as important to consider small details, like a fresh coat of interior and exterior paint, and landscaping. Buyers who want a move-in ready home will be more likely to see the full value of your home if they don’t have to stretch their imagination to see its potential.

How Can You Increase Your Home Value with Your Home Equity?

According to the CoreLogic Home Equity Insights report, U.S. homeowners with mortgages have seen their equity increase by 5.1% from the third quarter of 2018 to the third quarter of 2019. During that period, the average homeowner gained $5,300 in home equity. In fast-growing states like Idaho, the average homeowners’ equity increased $25,800 in that same period.

For many homeowners, these numbers point to a significant opportunity. By accessing your equity—whether via a home equity loan, home equity investment, or other means—you can get the cash you need to tackle home improvement projects, including more major renovations like building an addition or refinishing a basement. These home improvements can help you get top dollar for your home when you are ready to sell or simply increase the value of one of your largest assets. Compare options for accessing your equity to see what may make sense for you and your property.

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only.To determinethe best financing for your personal circumstances and goals, consult witha licensed advisor.

When interest rates drop, your first instinct may be to refinance. At the beginning of March 2020, the average interest rate for a 30-year, fixed-rate mortgage hit its lowest level in 50 years at 3.29%, and many homeowners jumped at the opportunity to lock in a new, lower mortgage rate. But are interest rates still low? As of March 2022, rates are unfortunately on the rise again — the current average for a 30-year fixed mortgage is 4.51% . It has many homeowners wondering: is it a good time to refinance my home before rates get even higher?

To answer the question, you’ll need to do some math. Most finance experts advise you to lock in a rate that’s at least 0.5% lower than your current rate to make a refinance worth it. But refinancing isn’t as straightforward as simply locking in a new, lower interest rate. You’re taking on a new loan, and new loans come with closing costs. Expect to pay 2 to 5 percent of the loan’s principal to refinance, with fees varying by state and lender. The general rule of thumb is you should be able to recoup closing costs within 18 months.

How to Know When to Refinance

To determine whether it’s a good idea to refinance, you’ll want to take into account all the variables of your situation. If you shorten your loan term, will you pay less interest in the long run? If you trade one 30-year mortgage for another, will you pay more interest in the long run? Can you afford the monthly payment? Can you switch from a potentially volatile variable interest rate to a fixed rate that helps you budget more effectively? Can you eliminate private mortgage insurance (PMI)? How long do you plan to stay in your home before selling? If you refinance your home before selling it shortly after, it may not be financially beneficial for you since you’ll have to deal with closing costs.

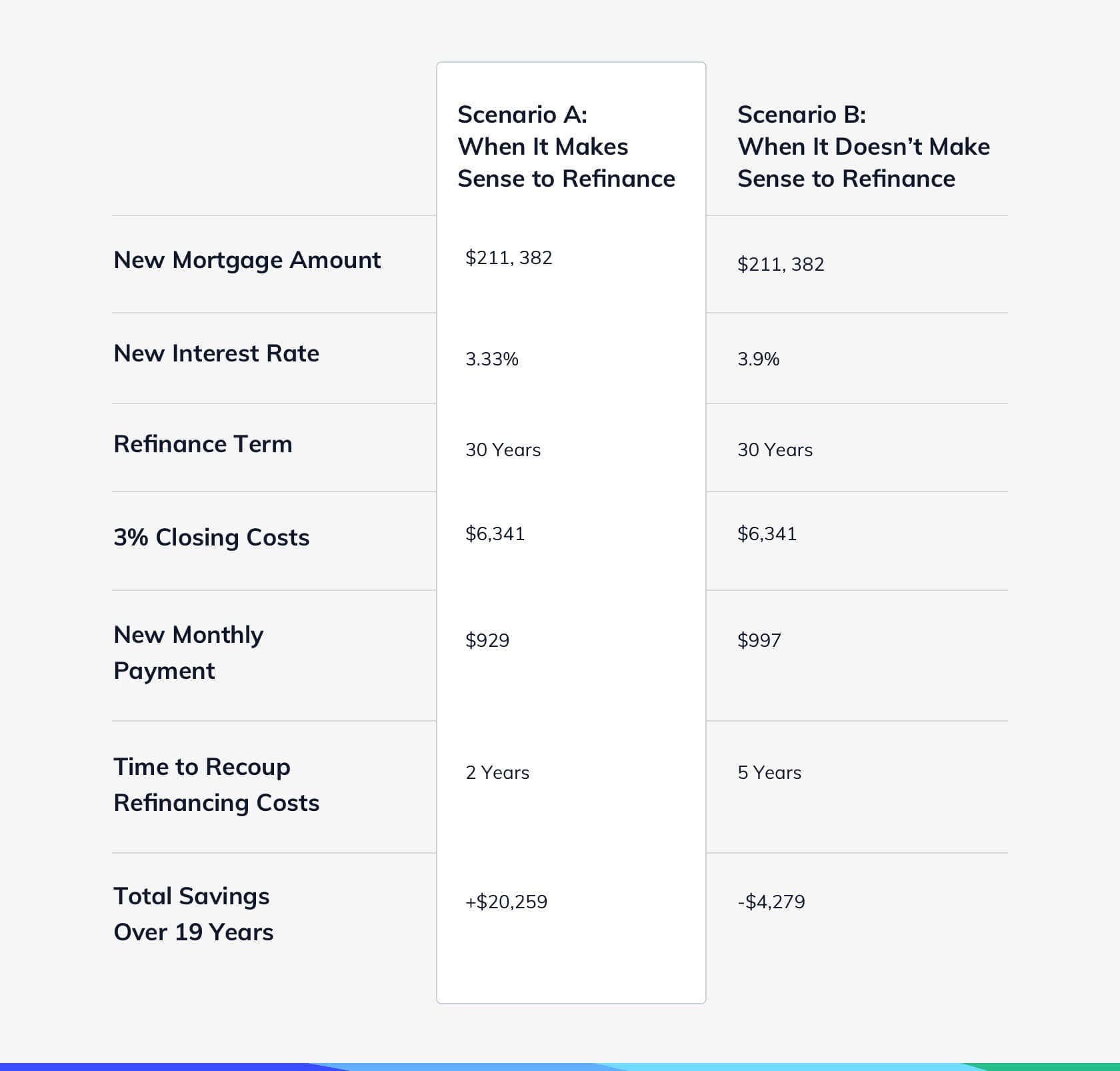

As an example, let’s say you bought a home in 2009 that’s currently valued at $300,000. Your initial 30-year mortgage was for $275,000 at a 4.25% interest rate. That leaves $211,382 left to pay off at $1,495 per month (factor in more if you’re paying PMI).

In scenario B, due to the length of the loan, you stand to pay more in interest. If you plan to move between years five and thirteen, you could save a few hundred dollars, but the hassle of refinancing is likely not worth the savings.

Opting for a 15-year loan over a 30-year loan in this scenario would increase your monthly payments to $1,553, but you could save nearly $12,000 over the lifetime of the loan, making it a slightly more attractive refinancing scenario. You’d recoup your refinancing costs around year three. Should You Refinance Your Home? 5 Key Areas to Evaluate

Of course, you’ll also need to look at the specific qualification requirements to determine if you meet the criteria for a refinance. While they vary by lender, these generally include a minimum credit score of 620, a 50% debt-to-income (DTI) ratio, and at least 20% equity in your home.

The SmartAsset Refinance Calculator is a great tool for homeowners to see when it may make sense to refinance their homes based on the home’s current value and mortgage.

With refinancing, you’re taking out a new loan for the remaining value that you owe on your home, ideally reducing the amount you have to pay each month, the amount of time left to pay the loan, or both.

But with a cash-out refinance, you’re taking out a new loan that’s greater than the amount you owe on your home, giving you additional cash to cover other expenses you may have, such as credit card debt or paying for an education. Cash-Out Refinance vs. Home Equity Loan: What’s the Difference?

But, if you don’t want a larger loan and potentially even larger monthly payments, you also have non-loan options. Home equity investments allow you to access cash now in exchange for a share of the future value of your home. Since it’s an investment, not a loan, a home equity investment doesn’t have monthly payments or interest.

Home equity investments may make even more sense for homeowners looking to sell within the next decade, or before they can realize any savings from a refinance. A refinance can extend the lifetime of your loan. If you had 20 years left on your mortgage, and you refinance with a 30-year mortgage, you have 10 additional years of monthly payments and interest).

The best option for you will depend on a number of factors, including your home plans, credit score, and other variables. But it also depends on your other financial goals. What do you hope to do with your savings from a refinance? Do you need cash now to achieve another financial goal, such as pay off bad debt or start a business? Do the math, weigh all your options, and determine which scenario is best for you.

Take our 5-minute quiz to see if a home equity investment is a good fit for you.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

This article was last updated on February 10, 2023.

The IRS has an entire decade to collect your taxes. So, whether you owe $5,000 or $50,000 it’s best to start paying down your bill as soon as possible. Avoiding payment can lead to the IRS taking money directly from your wages or bank account, or even putting a federal tax lien against your property, which may impact your ability to take out loans, access your home equity, and more.

If you owe money this year or from prior years—don’t panic. Here are some important updates and options to get your finances back on track.

What’s New for 2023 Tax Season (for the 2022 tax year)

Important Tax Dates:

April 18: Filing deadline for most U.S. residents

October 16: Filing deadline if you were granted an extension

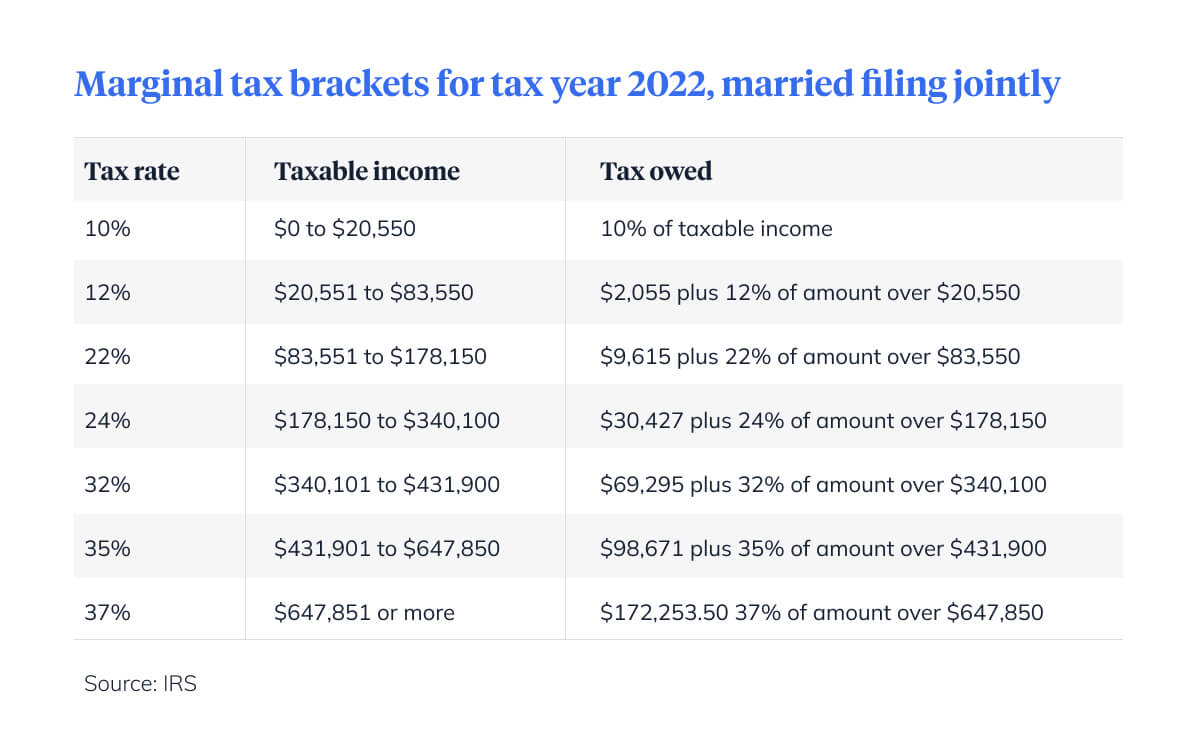

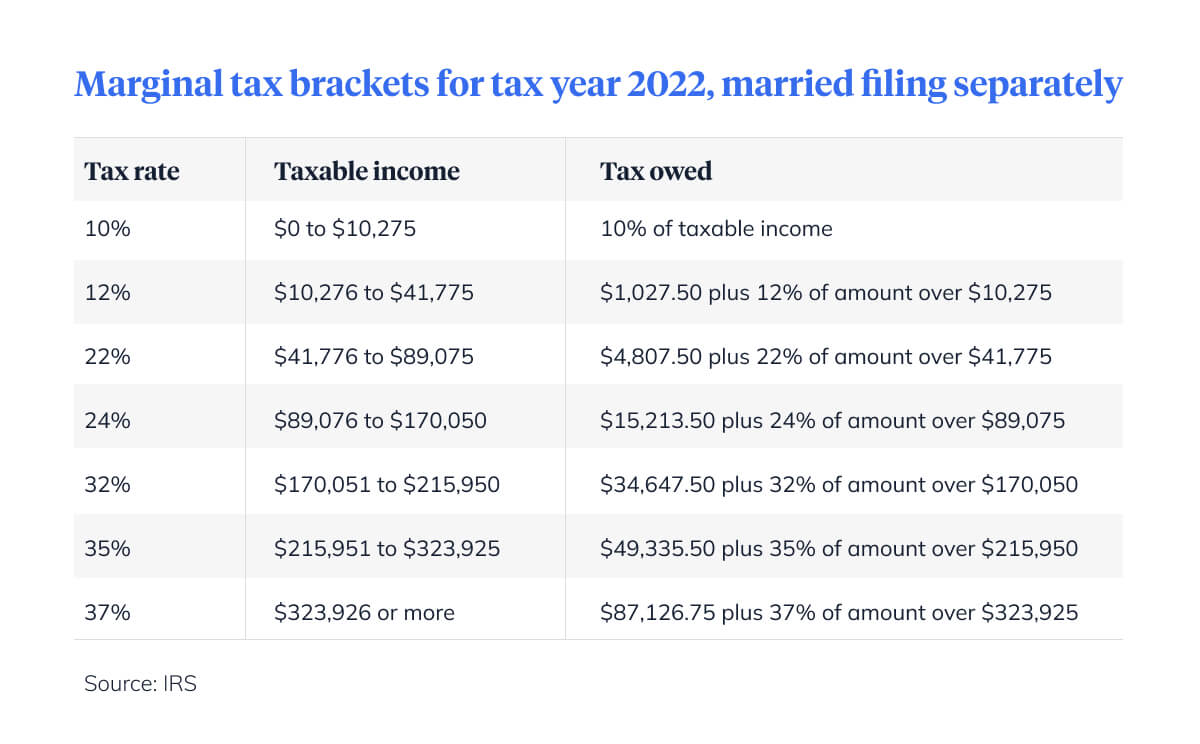

2022 Tax Bracket Updates

The federal income tax brackets have changed for 2022, so your first step should be understanding what bracket you fall into this year.

Form 1099-K Reporting Changes

If you received any third party payments in 2022 for goods or services that exceeded $600, you’ll get a Form 1099-K for payment card and third party transactions that you’ll need to fill out. However, personal reimbursements or gifts from family or friends received through third party platforms are not taxable. In previous years, Form 1099-K was only issued if a taxpayer completed more than 200 transactions in a year that totalled more than $20,000.

Smaller Returns

Overall, largely due to the scaling back of tax credits to 2019 levels — including the Child Tax Credit, Earned Income Tax Credit, and the Child and Dependent Care Credit — you can expect a lower return than in previous years.

No Above-the-Line Charitable Deductions

Another change for the 2022 tax season is that taxpayers are no longer able to deduct up to $600 for charitable donations like they were in 2021.

Premium Tax Credit Updates

While many of the adjustments for this tax season have restricted or narrowed eligibility and credit amounts, the premium tax credit may actually be available to more 2022 taxpayers due to the expanded criteria. For 2022, to be eligible, you must:

You may be eligible for a nonrefundable credit of up to $7,500 if you purchased a qualifying, new plug-in electric vehicle for your own use in 2022 or prior.

Child Tax Credit Updates

For the 2022 tax year, the child tax credit has reverted to $2,000 per child under age 17 who is claimed as a dependent on your return. Note that if your modified adjusted gross income (AGI) exceeds $400,000 on a joint return or $200,000 on a single/head-of-household return, your credit amount will be reduced by $50 for each $1,000 you earn beyond this threshold.

Finally, the credit is no longer fully refundable in most cases — except for select lower-income taxpayers, for whom up to $1,500 may be refunded.

If you owe more than you expected this tax season, there are a few things you can do to alleviate the financial burden.

1. File—Even if You Can’t Pay in Full

As you get ready to prep your 2022 taxes—and any back taxes you still need to file—remember that filing can help reduce the amount of money you owe in the long run. As H&R Block notes, the IRS imposes a hefty “failure to file” penalty, equal to 5% of the unpaid balance each month, up to 25% of your unpaid taxes. With the added penalties, that means the interest accruing on your unpaid taxes will be higher, too.

2. Request an Extension

If you need more time to organize files for your taxes, or come up with a game plan because you know you owe more than you can pay, you can file for a six-month extension.

While filing an extension for your 2022 taxes doesn’t buy you more time for paying taxes (you still need to estimate the amount you owe and pay it), it does ensure you won’t begin to accrue late-filing or late payment penalties right away. As TurboTax explains, “if you pay less than 90% of the tax you owe, you’ll end up owing a penalty of 0.5% of the underpayment every month” until your balance is paid.

3. Explore IRS Payment Options

The IRS allows multiple options for paying your taxes. You may even be able to temporarily delay collection of your taxes based on your financial situation. You can also set up a short- and long-term payment plan. Each has an application fee that varies depending on your plan and financial status. However, note that interest and other penalties that will continue to add up for either of these options as long as you have an outstanding balance. The IRS interest rates are subject to change quarterly.

Another option may be to file an Offer in Compromise that allows you to settle your IRS debt for an amount that’s less than the total you owe. If you’re a homeowner, you may find your home — likely your biggest asset — disqualifies you. Since you have equity in your home, the IRS sees that as means to pay your taxes.

4. Access Your Home Equity to Help with Taxes

Not paying your taxes can result in a lien on your home, making it harder — if not impossible—to access your home equity. But you can access your home equity to settle your debt before a lien is placed on your home.

Paying off your taxes with a home equity loan, especially if you owe more than you can pay off in a single credit card payment, allows you to avoid taking on bad debt. Unlike credit cards that average more than 16% interest, a home equity loan only averages 5.82%. When you file, you’ll know the lump sum you owe, which may make a home equity loan more appealing than a home equity line of credit (HELOC). With either, you’ll want to make sure you can afford payments, as you risk foreclosure if you can’t make your payments.

Note that following the 2017 Tax Cuts and Jobs Act, the interest you pay on a home equity loan or HELOC is no longer tax deductible if you use it for paying off taxes. Interest on these loans, as U.S. News & World Report explains, only qualifies for a tax deduction if you use the loans to make home improvements.

Another option is accessing your home equity via a home equity investment. Unlike a loan, a home equity investment gives you cash now in exchange for a share of the future value of your home.

Since it’s an investment, rather than a loan, there are no monthly payments and there is no interest. Instead, you settle the investment when you sell your home or buy out the investment. Plus, with home equity investments from companies like Hometap, your debt-to-income ratio isn’t a qualification factor as it is with home equity loans.

You should always do the research and the math to find out which payment method works best for your financial situation. You may find accessing your equity is a more affordable way to pay off your taxes than the IRS payment plan—or vice versa.

See if you pre-qualify for a Hometap Investment in less than 30 seconds.

YOU SHOULD KNOW…

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

So your child got into their dream school. Congrats! They’re happy, you’re happy, years of hard work have finally paid off. Then you review the financial aid package and—cue cold sweat—they expect you to pay how much?

With the cost of college rising faster than financial aid awards, many parents and students are facing the seemingly impossible choice of taking on massive debt or forgoing a dream school for a lower-cost option. And, as it turns out, your home equity could be a factor.

What does my 3-bedroom have to do with a degree?

First the good news: not all schools take your home equity into account when calculating aid. If your child chose a school that only requires the FAFSA form, your equity won’t count against you. But, if they hope to attend one of the roughly 200 schools that also require the CSS profile, it’s almost certain some percentage of your home equity will be factored into financial aid.

Exactly how much is hard to say. Some schools take 100% of your equity into account, while others cap it based on income. Either way, it could lower your aid package.

Let’s say you have $100,000 in equity. Parent assets are assessed at 5% in the CSS profile, so that would raise your expected contribution by about $5,000.

Okay. But cashing in on my home equity isn’t so simple.

One reason for this is lingering anxiety over the recession. Home Equity Lines of Credit (HELOCs), a once-popular type of loan used to fund education, have fallen by almost half in the past decade despite overall equity growth. Families are reluctant to borrow against their home value—and for good reason. If you default on a HELOC, you could lose your home.

Selling is another option, but for most families it’s not a realistic one. After all, you need a place to live (and we’re pretty sure your child won’t appreciate it if you move into the dorm with them).

So, what CAN I do?

Short of withdrawing your child’s application from schools that require the CSS profile, there’s not much you can do about your home equity being factored into financial aid. But there are ways to turn your home’s equity into cash—without risking the loss of your home.

Some parents opt for a cash-out refinancing—when you take out a mortgage for a larger amount than the existing loan in order to get cash back. Today’s comparatively low interest rates make this more attractive than HELOCs, though, naturally, this increases your debt.

Another option is a home equity investment. An investor provides cash in exchange for a share of the future value of your home. This allows you to tap into your equity without any debt or monthly payments. And when the time finally comes to drop your new college student off at the dorm, do it knowing you’ve made the best financial decision for you and your family.

See if you prequalify for a Hometap investment in less than 30 seconds.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

With equity built up in their homes but little to no cash on hand for more immediate expenses, 79 percent of Boston-area homeowners feel house rich and cash poor, and 22 percent of those feel this way most or all of the time, according to a recent Hometap study of Boston-area homeowners.

Massachusetts ranks No. 5 on the list of costliest monthly mortgages in the U.S., at $1,333 on average. It also comes in at No. 5 on Porch’s list of highest annual home maintenance costs, averaging $17,461.

It’s no wonder, then, that the top stressor for Boston homeowners, based on our survey results, is the cost of home maintenance. Eighty-one percent of those surveyed answered that they’re moderately to extremely stressed when factoring this potential cost into the big picture of homeownership.

What’s the True Cause of the Stress Behind Homeownership?

Since its infancy, Hometap has been studying the house-rich, cash poor phenomenon that has been building since the Great Recession. The widening gap between wages and housing costs as well as the lack of attractive options to access home equity is largely to blame for this crisis. In fact, according to our study, 71 percent of Boston-area homeowners report their housing costs are rising faster than their income while 62 percent say they’re spending a higher percentage of their income on housing than ever before.

Why Does It Matter?

Our study of nearly 700 homeowners nationwide aimed to track the impact the house-rich, cash-poor crisis is having on homeowners across the country. What we found when we took a closer look at Boston was that the security of future income, property taxes, and maintenance costs are the greatest sources of this stress.

See the national results of Hometap’s Homeowner Study

Property taxes are a moderate contributor of stress across much of the country, but in certain areas, including Boston, it’s a more significant source of stress (75 percent answered they’re moderately to extremely stressed, compared to only 54 percent nationally).

74 percent expect the gap between wages and housing costs to increase—not an unreasonable fear when you consider what homes are going for today. A 2018 Boston Magazine article claimed that just to rent in Boston requires a minimum annual salary of $78,477 (without roommates). The median household income in the Boston-Quincy area in 2017 was not too far beyond that at $85,691. Bostonians overwhelming answered (73 percent) that they’re moderately to extremely stressed about security of future income—and 15 percent aired on the side of ‘extremely.’

Access Your Equity, Eliminate Homeowner Stress

The vast majority of Boston-area homeowners (88 percent) said they believe they’re building equity in their homes, and there’s a good chance they’re right. Thanks to growing demand to be in Boston, home values are skyrocketing; the Boston Home Price Index increased 118 percent between 2000 and 2018 (compared to a 95 percent increase nationally).

But 64 percent of Boston-area homeowners say high housing costs make it difficult to achieve other financial goals, whether that’s paying off debt, starting a small business, or any number of goals. Nearly as many (63 percent) don’t feel like they have good options for turning the equity in their home into cash.

Twenty-five percent don’t want to take on a loan and the debt, interest, and monthly payments that come with it. Another 25 percent say they could sell their home to access equity but would prefer not to.

As a homeowner, you do have options. You can access home equity via a home equity loan, home equity line of credit (HELOC), cash-out refinance, or home equity investment—and not all of these options involve taking on additional debt.

LEGAL DISCLAIMER

The opinions expressed in this post are for informational purposes only. To determine the best financing for your personal circumstances and goals, consult with a licensed advisor.

If you’re refinancing your home, or looking at home equity loans, home equity lines of credit (HELOC), or home equity investments, your lender will likely require a home appraisal. But there are other reasons you’d want an appraisal, too, such as wanting to know a fair asking price when selling, or proving you have enough equity in your home to eliminate private mortgage insurance. But can you find your home value on your own?

Before you rush to schedule a home appraisal, also called a home value appraisal, consider the cost: upwards of $400 for single-family homes, according to Angi. That’s why many homeowners turn to sites—such as Zillow or Redfin, among other automated valuation models (AVMs)—to predict their current home value appraisal estimate. However, while AVMs may give you a rough idea of your home’s value, it’s not always the most accurate, as these websites often rely on public and user-inputted data.

In fact, a recent experiment from BiggerPockets illustrates just how unreliable Zillow’s “Zestimates” can be compared to actual house appraisals:

As you can see, the margin for error can be as high as 30%!

While you can compare multiple sites to get a better sense of an average, or use a lender-grade AVM, you can also crunch the numbers yourself to determine the appraisal value of your home. Follow these three steps to decide whether to order a professional appraisal now or wait until the timing is right.

Discover how many U.S. homeowners don’t know how much home equity they have. Our 2021 Homeowner Report is out!

How to Find Your Home Value in 3 Steps

1. Find Nearby Comps

Comps, short for comparables, are homes that are similar to yours in location, size, acreage, floor plan, bed and bathroom counts, and more, that have recently sold. Definitions of “recent” vary, particularly in areas without much market activity, but try to find homes sold no more than 60 days ago. Selling prices of comps have a major impact on your home’s value. Investopedia recommends looking at homes that are within 300 square feet of your home’s square footage.

In terms of location, NerdWallet recommends the closer, the better. It’s not about the same zip code, but rather the same school district, neighborhood, and even street. If possible, visit the homes in person. Photos online may not tell the whole story, such as if the property is on a noisy street, if it’s in need of repairs, or if it has features like an in-ground pool.

Look at sites like Realtor.com to find homes similar to yours. Look for “just sold” properties, as homes still on the market will show asking prices; the home may sell for more or less. You can also ask a real estate agent for a comparative market analysis to see nearby selling prices of homes. These reports are often low cost or free, but the agent may anticipate working with you if you decide to sell.

2. Find the Cost-per-square-foot

While some listings may have the price by square footage, some may not. You’ll want to take the selling price and divide by the square footage to find the price-per-square-foot. For example, a 2,500-square-foot house that sold for $400,000 is $160 per square foot.

Look at several properties, at least three if possible, and get the cost per square foot of all homes.

3. Determine Your Range

Add up the cost per square foot of all the homes you looked at and divide by the number of homes to get the average cost per square foot. Take this number and multiply it by your home’s square footage.

You’re not quite done yet. With this information, give yourself a range of 10 percent in either direction, as home values can quickly change based on nearby comps and the supply and demand of the housing market.

10% = .10 x 385,000 = 38,500

385,000 + 38,500 = 423,500

385,000 – 38,500 = 346,500

Your estimated home value appraisal range = $346,500 – $423,500.

How to Increase Your Home’s Value

If you’re not thrilled about your home’s appraised value, there are ways to increase it. Certain repairs have a greater return on investment than others, such as garage door replacement or a new roof. But your upgrades don’t have to break the bank; consider smaller renovations like a fresh coat of paint or increasing your home’s curb appeal with a power wash and updated landscaping.

Our free Equity Increaser Guide is designed to help homeowners not only maintain, but grow their home value over time.

Certain home renovations may require more funding than you have on hand. With a home equity investment from a partner like Hometap, you can get the cash you need now to make home renovations in exchange for a share of the future value of your home.

See if you prequalify for a Hometap investment in less than 30 seconds.

YOU SHOULD KNOW…

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.